01 May 2008 Conservation Easements: The Good, the Bad, and the Ugly, by Dana Joel Gattuso

Introduction

Conservation easements, as we know them today, are a fairly recent approach to land conservation. As government acquisitions and regulatory restrictions on land use have become prohibitively invasive, costly, and ineffective, governments have looked to conservation easements as a potentially effective and less expensive conservation method than government ownership and/or regulation. Use of conservation easements began to gain steam by the 1980s and by the 1990s, exploded on the scene.

Initially, conservation easements – which allow landowners to hold on to and use their property but permanently remove development rights in exchange for tax benefits – seemed to hold some promise as an unintrusive, effective means of preserving open space while upholding private stewardship, private initiative and the rights of private property owners. Land trusts, the organizations that manage the easements, tended originally to be small, nonpolitical, and independent of government involvement.

Over time, however, as numerous land trusts have grown in size and number, so have their association – and influence – with government. This has been the case particularly with the large, national organizations that obtain enormous sums from federal funding. For many of these land trusts, what used to be a close working relationship with private landowners has been replaced by a closer relationship with government agencies. Increasingly too, the mission has evolved from protecting open lands through private stewardship to aiding government agencies in acquiring private lands. In these troubling arrangements, land trusts have operated more like government agents, acquiring easements from private landowners, only to turn around and quietly sell them – sometimes for a profit – to state or federal governments. These methods certainly are not practiced by all land trusts, but nor are they isolated cases.

Given the rapid growth in land trusts and the rising use of conservation easements over the past decade, along with increasing involvement with government in the arrangements, easements could become a far-reaching means for public land acquisition. That is, easements, absent reforms, could evolve into the prevailing method for government to shift lands unobtrusively from private to public control under a pretense of private stewardship.

Other problems too have evolved. Federal tax incentives for conservation easements require landowners to encumber their land in perpetuity. While the permanency may hold appeal to those property owners who see value in shielding their land from developers forever, particularly when sweetened with a significant tax deduction, it could prove to be detrimental to the public over the long-term as economic and ecological factors change our definitions of what should be preserved and why. Because conservation easements essentially are a contract between two people – the grantor and the grantee – one of the promising aspects of easements has always been their flexibility and adaptability, compared to government ownership and regulations. Perpetuity requirements run counter to flexibility and necessary change.

The tax incentives themselves also are problematic, developing into what some critics call a “tax haven” and “tax bonanza” for the wealthy landowner. Although the tax benefits were intended to aid the land-rich, cash-poor farmer or small business, struggling because of exorbitant property and estate taxes to hold on to their land, the federal tax benefits disproportionately favor wealthy landowners.

This report examines these issues, addressing 1) conservation easements’ evolution from a promising approach aimed at protecting land through private ownership to a questionable arrangement that shifts private lands to government control; 2) the costly and potentially detrimental impact of perpetual deeds; and 3) the manipulative use of the tax code.

Policy reforms can change conservation easements as we know them today, returning control of land to property owners while removing existing disincentives to land preservation. Among these are:

* Preventing government takeover of land through land trusts’ acquisition of conservation easements.

* Phasing out government funding of land trusts.

* Changing the tax code to allow for fixed-term, rather than perpetual, conservation easements.

* Eliminating estate taxes, which encourage property owners to sell their land to developers.

Background on Conservation Easements

A conservation easement1 is a legally-binding agreement between a property owner and a nonprofit organization – typically a land trust – or a government agency2 that restricts development on the land covered by the easement, usually in exchange for tax benefits for the property owner.3 The property owner who donates or sells the easement – called the “grantor” – retains partial ownership rights over the land but relinquishes rights to use the property for development.4 The organization to receive or buy the easement – called the grantee – holds interest in the property and enforces the restrictions.

Property owners typically are motivated to place their land in a conservation easement by deductions from federal and state taxes, by a desire to shield their property from development,5 or by the threat of government land-acquisition or land-use regulations.6 To receive tax benefits, landowners must agree to allow the land to be used for one of the following: outdoor recreation for the general public; protection of animals, plants or ecosystems; preservation of open spaces – for either farming, forestry, or ranching7 – or for scenic enjoyment for the general public; or the preservation of historic land or structures.8

They also must donate the easement to a government agency or a “qualified” nonprofit organization, defined as a charitable organization “that receives a substantial portion of [its] support from the public and government entities.”9 And they must agree that the easement will be held in perpetuity, meaning all future landowners of the easement are bound by the terms of the deed. The intended purpose of the easement is to preserve the land for the benefit of the general public.10

Birth, Growth, and Boom of the Conservation Easement

The earliest “conservation easement” of its kind dates back to 1891. The first private land trust, the Trustees of Reservations in Massachusetts, was formed to purchase and maintain public parkways, designed by landscape architect Frederick Law Olmsted, throughout the city of Boston. Conservation easements were not used again until the 1930s and 1940s, when the National Park Service bought parcels of land for scenic use along what are now the Blue Ridge Parkway and the Natchez Trace Parkway.11

This was the first instance in which a government entity managed land that wasn’t via fee simple ownership of the entire property.12 However, these “scenic easements” differed largely from today’s conservation easements in that they were primarily intended for public access and enjoyment of parks and vistas.13 Conservation easements as we know them today – designed to curb development – did not evolve for a few more decades.

Washington and states bolster the easement “movement.” In 1964, the Internal Revenue Service authorized the first rule allowing charitable income tax deductions to landowners who donated property for scenic easements adjacent to federal highways. A year later, as part of the Federal Highway Beautification Act, Congress required states to spend 3 percent of federal highway funds on landscapes and beautification along the highways as a condition of renewed federal funding.14 The requirement spurred states to enact enabling legislation for conservation easements.15 Today, all 50 states and the District of Columbia have enacted enabling legislation.16

Generally, the states followed the provisions of the Uniform Conservation Easement Act (UCEA), a non-binding, national blueprint for state legislation. The legislative template was drafted in 1981 by the National Conference of Commissioners on Uniform State Laws, a nongovernmental body that provides model legislation for states. The act recommended that states enact enabling legislation to address any existing impediments to traditional common law (discussed later in this paper). The draft also included model language stipulating conservation purposes of an easement, restrictions on which organizations are entitled to hold easements, and provisions allowing a “third party” to enforce an easement’s requirements.17 During this time, Congress provided incentives to landowners by codifying the IRS’ ruling, providing a charitable tax deduction off federal income taxes to donors of conservation easements.

As Washington and the states took steps providing incentives and statutory authority, the use of conservation easements gradually advanced. By the 1980s, the easements were used routinely; by the 1990s, they exploded on the scene.

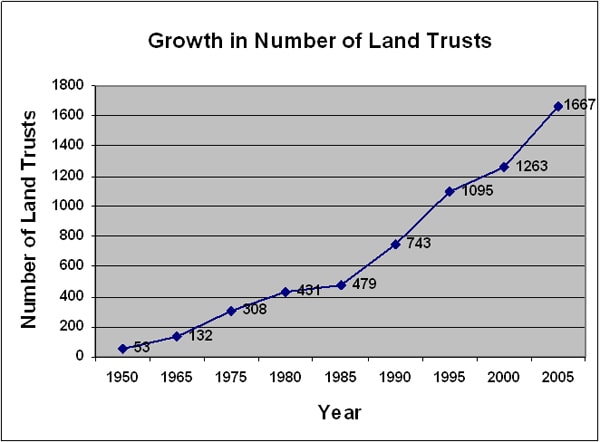

The surge in land trusts and conservation easements. The graph below shows the dramatic increase in the number of land trusts since 1950, particularly the last five years data is available, where the numbers rose from 1,263 in 2000 to 1,667 in 2005.

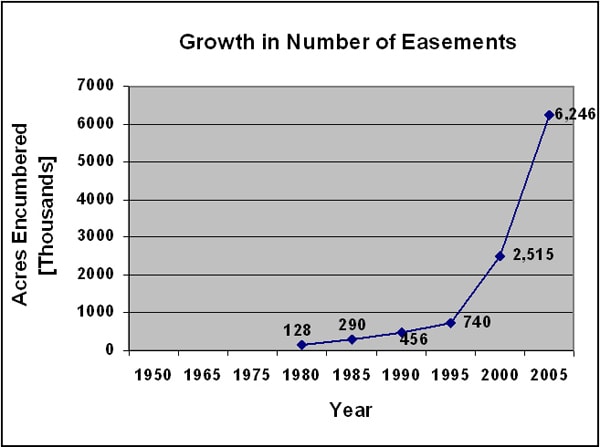

Collectively, land trusts control 37 million acres of land throughout the United States.19 At least nine million acres of this amount is believed to be held in conservation easements, though the precise amount is not well documented.20 As the following graph illustrates, the rise in the use of conservation easements has paralleled the growth of the land trust movement.

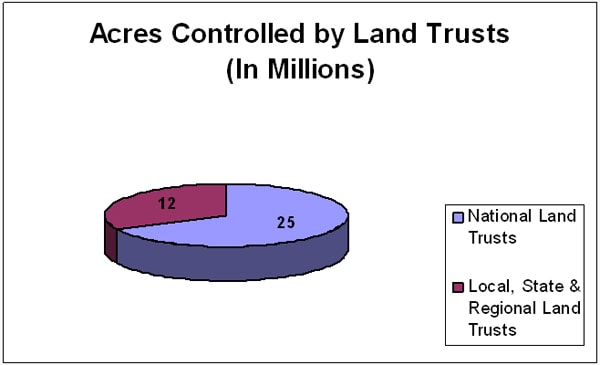

Most of the controlled land is managed by large, national environmental organizations, such as The Nature Conservancy, The Trust for Public Land, Ducks Unlimited, American Farmland Trust and The Conservation Fund. Together, they hold 25 million acres of land. The largest of these is The Nature Conservancy (TNC) which controls 15 million acres. Over three million acres is held in conservation easements by TNC, a fivefold increase since 1997, when the land trust held 645,000.22

The nation’s 1,663 local, state and regional land trusts control 12 million acres of private lands. Approximately half that amount – 6.2 million acres – is from conservation easements, up from 2.5 million acres in 2000.23

Explanations for easement zeal. The rapid growth and popularity of conservation easements as a conservation tool is partly a response to exorbitant costs of government regulations on land use and zoning laws. It is also an outgrowth of gradual public disapproval over the economic burdens that government “command and control” land use policies place on landowners.24

Many property rights advocates also argue the threat of land use regulations and federal land-grabs can act as an incentive for conservation easements, driving landowners to sell or donate a conservation easement to avoid the burden of a threatened regulation. Faced with the choice of government seizing your land or encumbering your land with a conservation easement, most landowners would, even if grudgingly, opt for the latter.25

Conservation easements’ growing use is also a factor of the overwhelming rise in number and influence of land trusts in the United States.26 As the number of land trusts has risen, so has land trusts’ choice for conservation easements over fee simple ownership as a conservation tool. Rising costs of purchasing land for conservation – reflecting the opportunity costs of leaving land dormant rather than developed – have made easements a more affordable and practical approach.27

Finally, the recent conservation easement phenomenon is due to a growing interest among property owners. Some researchers suggest landowners are driven to donate land for easements largely through their love of their land and their desire to keep it protected from development, both in the present and long after they are gone.28 Others believe tax relief is the driving force.29

Tax Incentives

There are two forms of federal tax benefits available to donors:

1. Federal income tax deduction

Because donated conservation easements are considered a charitable donation under the federal tax code, property owners can deduct the value of the easement, defined as the difference between the value of the land just before the easement is granted and the value of the land immediately after the donation. In August 2006, President Bush signed the revised Pension Protection Act, which raised the maximum federal tax deduction for conservation easements from a maximum of 30 percent of adjusted gross income to 100 percent for farmers and ranchers, and to 50 percent for non-farmers.30 The increase expired at the end of December 2007, but a provision now pending in the Food and Energy Security Act of 2007 (the “farm bill”) would extend the tax deductions for two more years.31

2. Federal estate tax deduction

Relief from estate taxes is the most significant tax benefit for landowners granting conservation easements, particularly those who inherit sizable estates. In 1997, Congress passed estate tax relief legislation for conservation easement grantors. The purpose was to encourage property owners to hold on to property they might otherwise want to sell to land developers to offset debilitating estate tax burdens. The tax provisions allow the grantor to deduct the value of the easement from the fair market value of the deceased’s estate. The donor also may deduct up to 40 percent of the value of the estate at the time the owner passes away.32

Most states also provide some form of tax incentive for conservation easements:

1. State income tax credits

Twelve states provide tax credits, though most are not as substantial as the federal income tax benefit. The most significant tax incentives are provided by Colorado and Virginia, which allow grantors to sell partial or full amounts of their credit to other taxpayers in the state.33

2. Property tax relief

At least 17 states also provide property tax incentives, allowing donors to deduct the value of the easement from the assessed value of the property.34

Achievements of Conservation Easements

Many commentators argue that conservation easements’ potential strength in preserving land is their approach as an alternative to government land acquisitions and land use regulations.35

Private land trusts, working closely with property owners to preserve the land through easements, have been known to be more effective stewards than government, and numerous studies bear this out.36 For one reason, land trusts are more flexible than government and more in tune with the needs of the community. Land trusts “promote a level of innovation and experimentation in private land conservation efforts that typically is not found in government controlled land conservation programs.”37 Furthermore, easements – when arranged on a purely voluntary and private basis, absent government involvement – can harness “the forces of self-interest to encourage the efficient use of resources,” as University of Virginia law professor Julia Mahoney writes, “rather than by using the power of the state to coerce individuals and institutions.”38

In fact, the oldest land trust in the United States was created as a response to what even then was regarded as the failure of government’s management of public lands. The Trustees of Reservations in Massachusetts was established in 1891 by landscape architect Charles Eliot, a protégé of Frederick Law Olmsted, to manage lands through private means. Eliot’s goal was to preserve small, tax-free parcels of scenic and historic lands in and around Boston for public enjoyment through private stewardship and voluntary means. Among the objectives was “to act for the benefit of the whole people, and without regard to the principal cause of the ineffectiveness of present methods, namely the local jealousies felt by townships and the parts of townships towards each other.”39

The scenic easements managed by the National Park Service in the 1930s and 1940s ended in failure only a few decades later. State agents, given the charge from the Park Service to acquire property from private landowners for the Blue Ridge and Natchez Trace parkway easements, failed to explain to landowners what rights they were giving up. As law professor Roger Cunningham writes in 1968, they were “concerned only with getting the landowner’s signature on the easement deed.”40 Nor were any appraisal standards applied. Landowners were paid drastically different sums from other donors giving similar land for scenic easements. Cunningham: “As a result, friction between the National Park Service and the… landowners increased; the number of violations steadily increased; and the cost of policing the scenic restrictions became substantial.”41 The problems and “numerous… conflicts that generated a mistrust of the use of scenic conservation easements by government agencies”42 forced the federal government to end its purchase of easements for the parkways at this time. It was government’s failure at managing scenic conservation easements, as well as its record on costly fee simple ownership, that gave birth and nurture to the private land trust.

While the voluntary arrangements of the Trustees of Reservations differed considerably from today’s conservation easements, it nonetheless set the stage for preserving parcels of land through private rather than public means. Today, the Trustees of Reservations manages 25,000 acres of land throughout Massachusetts, 14,000 of which is held in conservation easements.43 The organization has served for decades as a model to other private land trusts on how to preserve lands through private incentives, voluntary private property interests, and private stewardship.44

One such example is the Sand County Foundation, located in Wisconsin. The foundation dates back to 1965 and was established to preserve 120 acres of land located on the Wisconsin River floodplain, acquired by the 20th century ecologist and writer Aldo Leopold. The foundation’s founders wanted to utilize the approach espoused by Leopold, namely to protect property through “a conviction of individual responsibility to the land.”45 The founders sought the commitment from neighboring landowners to preserve the land and adjacent properties to commemorate Leopold and his “land ethic” on individual responsibility. Today, the foundation works with surrounding property owners to manage and conduct scientific research on 1,800 acres of private lands.46

Another example is the Montana Land Reliance in Bitterroot Valley, which protects land for agriculture use, fish and wildlife habitat, and open space. Holding more than 515 easements on 500,000 acres, the organization is the largest state-based land trust in the nation. Among its accomplishments are protecting elk, deer, and bears along the Madison River Valley adjacent to Yellowstone National Park. The land trust ensures easements remain in private control, maintaining that “private landowners make the best decisions for their land, given the right incentives.”47

Unfortunately, however, over time the focus of many land trusts has changed, and many of them – particularly the large national organizations – have developed suspect relationships with the government. In some cases, land trusts are aiding government agencies in obtaining private lands via conservation easements.

Problems with Conservation Easements

Stewards of Land or Stewards of Government?

Any chance conservation easements have in being effective stewards of land is lost when land trusts cease to work as independent, private organizations obtaining easements through purely voluntary means and become agents of government aiding in public land acquisitions. Yet land trusts, particularly the larger organizations, are changing their focus from independent and private approaches to working in tandem with government agencies in an effort to assist government in obtaining private lands.

In fact, many leaders in the land trust movement are articulating a new mission to pick up where government has failed at public ownership. As former president Jean Hocker of the Land Trust Alliance (the membership organization representing land trusts throughout the nation) observed, land trusts have a niche as a result of a “reluctance to regulate private lands or even to add land in public ownership.” And the “lack of a bureaucratic constraint makes land trusts exceedingly good at complementing, supplementing, and implementing public open-space agendas.”48

Prearranged “flip.” In increasing practice, land trusts do not hold on to the easement but turn around and sell it to federal or state government agencies, known as a “prearranged flip” or “preacquisition.” Because most easements are purchased by land trusts at below market value, land trusts can then sell the property to the government at market value, profiting off the difference. In one example, the Nature Conservancy bought an easement for $1.26 million, then directly sold it to the Bureau of Land Management for $1.4 million.49

Land trusts benefit because they can earn a profit off the taxpayer-funded arrangement. Government agencies like the arrangements because, unlike seizing private lands through land use regulations, zoning laws, or even eminent domain, they can obtain private property via methods shielded from public scrutiny. Preacquisitions also enable government to obtain private land when public funds are not yet readily available.50 As a report on easements by the Department of Agriculture notes, “voluntary acquisitions” provide “opportunities for public agencies to influence resource use without incurring the political costs of regulation or the full financial costs of outright land acquisition.”51

Preacquisitions change the whole nature, intent, and potential benefits of conservation easements to protect lands through private stewardship. As referenced earlier in this report, studies show that unequivocally easements work better when managed by land trusts than by government entities. Easements become not a means of protecting lands through a private sector partnership between landowner and land trust, but a non-transparent tool for government to obtain private property without public knowledge or approval. As Clemson University economics professor Bruce Yandle writes:

Such programs encourage land trusts to serve as government land agents, often quite profitably. If land trusts continue to respond to this temptation, land conservation will become ever more political…History teaches us that market incentives for conservation are strongest when individuals pay market prices and receive market rewards. They are weakest when government agents spend someone else’s money and get no reward for good management.52

While documentation is limited showing precisely how much land under conservation easement is transferred to government, anecdotal information indicates the practice is prevalent. An article published by the American Enterprise reports that more than two-thirds of the Nature Conservancy’s operating budget goes to purchasing private lands that are then sold to the government.53 Similarly, the national American Farmland Trust has worked closely with federal and state government agencies for years, leveraging tax dollars to turn private property into public land via the conservation easement. A book on land conservation “public-private partnerships,” published in 1993, describes such an arrangement with the state of Massachusetts:

Massachusetts has a strong tradition of private land conservation… Thus, it did not take much to convince the state agriculture department that a partnership with land trusts could enable it to save more Pioneer Valley farms than could the government acting alone. The department encouraged AFT [the American Farmland Trust] and other land trusts to acquire conservation easements over key parcels of valley farmland for subsequent resale to the state.54

The practice is also common among some state land trusts. The Maine Coast Heritage Trust, the state’s largest land trust along the coast, has sold more than 700 of its 850 easements and acquisitions to federal and state agencies. As described in the Gulf of Maine Times:

One of [the land trust’s] partners, the U.S. Fish and Wildlife Service (USFWS), identifies important habitats for migratory and endangered fish and wildlife. The trust works with the owners of these areas to determine if there is an opportunity to protect that habitat. If there is, the trust takes a lead role in acquiring the land on behalf of either USFWS or the Maine Department of Inland Fisheries and Wildlife.55

In some cases, the federal government uses partnerships with conservation groups to skirt existing state laws that limit the terms of an easement. A report released last September by the Government Accountability Office describes how the U.S. Fish and Wildlife Service has partnered with Ducks Unlimited to obtain thousands of acres of easements from private landowners in North Dakota.

The state forbids the term of an easement acquired by a conservation group to exceed 99 years.56 But according to officials from the Service, they are “not bound by state law regarding the easement terms.” If the agency “receives a monetary donation from Ducks Unlimited to purchase easements, the eased land is protected in perpetuity,” a direct violation of the state’s intent.57

Federal funding. Also indicative of the close “partnerships” many land trusts have with government is the amount of public funding land trusts receive, with The Nature Conservancy (TNC) collecting by far the largest amount of federal funds. The American Farmland Trust and The Conservation Fund take in a million and three million dollars annually in federal grants, respectively, while TNC receives an alarming sum exceeding one hundred million dollars. Moreover, revenues earned by TNC from sales of conservation easements to governments “and others” amounts to another $262 million annually, 20 percent of TNC’s support and revenues.58

Federal financing of conservation easements comes from numerous sources and programs, and it is difficult to find documentation showing the actual sum. However, it is clear that support has skyrocketed over the past decade. The two largest programs funding easements are the Forest Legacy Program and the Farm and Ranch Lands Protection Program, both operating under the U.S. Department of Agriculture. Funding for the Forest Legacy Program has ballooned from $2.6 million in fiscal year 1997 to over $80 million in fiscal 2007.59 The increase in the Farm and Ranch Lands Protection Program is even more dramatic, rising almost tenfold, from $62 million for 1996-2001 to $597 million for 2002-2007.60

Given the vast sums of federal dollars handed to many land trusts, along with the prearranged transfers of land from private hands to government acquisition, it is hard to imagine not only how land trusts can operate effectively as stewards of land, but also how they can operate independent of political pressures and influence.

Perpetual Conservation Easements: Forever Is a Long Time

Another problematic aspect of conservation easements is the requirement that the easement be held in perpetuity in order for the grantor to receive federal tax benefits.61 Such restrictions have ecological and economic implications to the public interest – the intended beneficiary of conservation easements – that extend far into the future. Furthermore, it is not fully clear how future courts will rule on the “dead-hand” control over private property.

Changes in science and nature could deem perpetual easements useless or harmful. As numerous legal scholars and policy experts have argued, conservation easements that bind landowners and their descendants in perpetuity ultimately become antiquated and, therefore, useless or even harmful. The rule fails to recognize that conservation needs – as well as definitions of scenic, aesthetic and cultural62 – change over time, and that the easement may eventually lose any ecological benefit or even become a detriment.

Gains in scientific knowledge can change our definition of what is ecologically beneficial. For example, we know from scientific advances in forest management that thinning techniques are essential to protecting healthy forests and their habitat and preventing forest fires.63 Yet conservation easement requirements with the specific purpose of perpetually protecting habitat in a forest may not allow for necessary logging and thinning projects.

In addition to gains in scientific knowledge, nature constantly affects changes that aren’t predictable. The very notion that easements in perpetuity are ecologically beneficial contradicts modern views in ecology which hold that the environment is “in a process of constant change rather than in search of a stable end-state.”64 For example, a conservation easement intended to protect the habitat of salmon would likely designate an area along a river for spawning and limit development. But rivers change their course over time. If the area under easement is defined geographically, it will be deemed useless when, inevitably, the river shifts.65 Another example would be a situation where a conservation easement covering a wetland to protect habitat dries up, deeming the wetland useless for conservation purposes. In still another situation, an easement created and written to protect an endangered species could become useless if the species becomes plentiful or extinct.

Some environmental lawyers respond that inevitable changes can be broadly addressed by writing “dynamic” – rather than the more traditional “static” – conservation easements. They recommend that perpetual easements be written specifically allowing for changes in science, nature, and public policy.66 But, as some of these same attorneys point out, drafting these easements can be prohibitively expensive and difficult to write, particularly for the smaller land trusts with limited staff and resources.67 And without possibly knowing or being able to predict what changes would occur, how could even the most experienced attorneys write an easement comprehensive enough to cover all possible changes to what’s considered ecologically beneficial, far into the future?

Another unintended consequence of perpetual conservation easements is the long-term impact they inevitably will have on housing costs. The rapid rate land trusts are acquiring properties, preventing construction of homes far into the future, will in time limit housing availability and push prices up.68 This already is a critical issue in California, where 427,000 acres of land are encumbered by conservation easements69 and where the state contains some of the most expensive real estate in the nation. For decades there has been a constant struggle pitting farming and grazing needs and the desire for open spaces against housing needs.70 With the rapid pace that land throughout the state is being taken out of production by conservation easements, housing costs can only be expected to rise further.

Does perpetual have to mean forever? Does a perpetual conservation easement allow either party to terminate the agreement once it has lost its ecological benefit? How difficult is it for heirs to terminate a time-worn agreement? And how costly?

The answers are not obvious, mainly because conservation easements do not conform to the traditional rules of common law (see next section).71 Outcomes could differ depending on the specific language of the easement, state law, and interpretations of the residing courts. Laws generally favor honoring perpetuity, primarily because grantors receive federal tax benefits for donating or selling conservation easements only if they are perpetual.

Land trusts particularly are motivated to ensure perpetuity, not only by a desire to maintain interest in the property far into the future, but also to assure prospective grantors that the property under easement will be protected forever.72 Furthermore, as some experts argue, land trusts are acutely aware of the inevitable future challenges to easements by descendants and are writing agreements they believe will survive the test of time.

The issue becomes less clear, however, in cases where the land trust, as well as the landowner, are in agreement over the need and desire to end a conservation easement. In these instances, the ease or difficulty generally depends on the state’s law governing easements. Most state laws either contain the same language in the non-binding Uniform Conservation Easement Act, stating the conservation easements may be modified or terminated “in the same manner as other easements,” and that courts may “modify or terminate a conservation easement in accordance with the principles of law and equity” – or they do not address the issue.73

But most experts agree state requirements and procedures for termination are not uniform, adding to the confusion over if, when, and how a perpetual conservation easement can be ended or modified.74 Some states require a public approval procedure.75 Other states stipulate the decision-making falls on the state attorney general, who enforces the general interests of the public.76

Legal scholars generally believe it is not likely that the courts will readily allow termination unless they determine the purpose for the conservation easement has changed or become obsolete, and the agreement no longer provides intended benefits. Specifically, courts can apply the Restatement (Third) of Property which reads, “[i]t is inevitable that, over time, changes will take place that will make it impracticable or impossible for some conservation servitudes to accomplish the purpose they were designed to serve. If no conservation or preservation purpose can be served by continuance of the servitude, the public interest requires that courts have the power to terminate the servitude so that some other productive use may be made of the land.”77

Regardless of the outcome, attempts to change perpetual conservation easements will be costly. If changes are sought by future descendants, legal and transaction fees are likely to be hefty. The law was written recognizing that the donor received tax benefits for agreeing to perpetuity. However, as the law now stands, in cases where termination is desired by both parties and the state or court allow it, the landowner would not be required to compensate the land trust. But if the property eventually is sold by the property owner, he would be required to pay the land trust a portion of the proceeds, assuming the owner initially received a charitable deduction.78

In conclusion, considering the rapid growth in the use of conservation easements, the question of perpetuity enforcement will be with us for decades to come and eventually must be dealt with by the courts in one way or another. And it will be costly. As law professor Julia Mahoney observes, perpetual conservation easements inevitably will burden future generations with economic, “ecological, legal and institutional messes for later generations to deal with.”79

Are perpetual conservation easements inconsistent with common law? Most legal experts agree that conservation easements, perpetual or time-limited, are not recognized under common law. Conservation easements are called “negative servitudes” in legal terminology, referring to the fact the easement holder is preventing the landowner from taking action on his own property – i.e., building or developing. By contrast, an “affirmative servitude,” or non-conservation easement, enables the landowner to make active use of his land. Common law, which favors use of one’s land rather than restrictions, traditionally recognizes only three types of negative servitudes, none of which include those for conservation purposes.80

In addition, conservation easements are easements “in gross,” meaning they benefit one or more individuals who do not own land adjacent to the easement. In a standard non-conservation easement, such as an agreement that allows the holder to use the grantor’s property to build an access road, the individual benefiting from the easement is the holder who owns land adjacent to the land under easement. In a conservation easement, however, the easement is assumed to benefit the general public, and does not entail ownership of adjacent land. Generally, common law has disfavored easements in gross and, specifically, has rejected long-lasting easements in gross. It has also rejected both covenants (contracts) and servitudes that bind holders of land via dead-hand control.81

Over the years, however, all 50 states and the District of Columbia have enacted laws allowing for perpetual “negative servitudes in gross.”82 While the laws vary from state to state, most include: 1) a legislative declaration of policy; 2) an authorization to utilize conservation easements as “property interest,” more apt to be recognized under common law, rather than as “covenants” or “contracts;” and 3) an attempt to shield conservation easements from common law doctrines.83 While some legal experts are of the view that in time, the courts will strike down the “perpetual” aspect of conservation easements, others believe that because statutes supersede common law, state laws allowing for perpetual easements will prevail.84

Tax Incentives

Another controversial aspect of conservation easements are tax incentives.85 From the viewpoint of the owner donating an easement, the tax benefit is pivotal; it is considered by many the key incentive driving the landowner to donate the use of his land.86 As noted recently by The Wall Street Journal, the increase in the federal income tax deduction for easement donations “spurred a sharp increase in the number of landowners interested in placing easements on their property.”87

Yet to some critics, the tax incentives are considered a “tax bonanza,” largely rewarding wealthy landowners and costing the U.S. Treasury over $1 billion, while providing questionable public benefit.88 Easements received wide public attention following a series in The Washington Post in 2003, exposing significant abuses and violations by land trusts, most notably, The Nature Conservancy. The articles revealed a typical practice in which the land trust acquires an easement for millions of dollars, then turns around and sells it at a loss for a considerable tax write-off. In some cases, easements had little to do with conservation, such as using the tax-funded arrangements to build golf courses.89

The series triggered a Congressional investigation, followed by a 2005 report by the Joint Committee on Taxation, concluding that current tax policy also enables “taxpayers to claim substantial charitable deductions for conservation easements that arguably do not serve a significant conservation purpose.”90 Similarly, the report found that the process for appraising the value of the easement is ripe for error, and that the subjective nature of assessing the value of the easement before and after the donation makes it “virtually certain that many appraised values are incorrect.”91

The IRS since then has cracked down on such activities and unlike previously, now audits conservation easement donations routinely. Furthermore, the Land Trust Alliance is working closely with its members on proper and ethical handling of easements. In 2004, it revised its “Land Trust Standards and Practices,” devising new accounting and ethical procedures and requiring its members to adopt the new policies. In 2005, it introduced an accreditation program for conservation groups and worked closely with the Senate Finance Committee to adopt new uniform appraisal standards and rules on conflict of interest.92 Furthermore, a new law enacted in 2006 tightens the rules governing appraisals and establishes harsh penalties.93

But reforms have not changed another problem with the tax incentives – what many view as conservation easement’s unfair tax treatment of non-wealthy property owners. Because the allowable charitable income tax deduction is based on annual income, individuals in high income brackets earn disproportionately larger tax savings than those in middle and lower.

As an example, consider three individual grantors with different income levels, each donating a conservation easement worth $500,000. The grantor with an adjusted growth income of $35,000 will receive an annual charitable tax deduction of $10,500, an aggregate tax deduction over six years of $63,000, and an aggregate tax savings of $9,450. The individual earning $75,000 receives an annual deduction of $22,500, a deduction over six years of $135,000, and an aggregate tax savings of $36,450. A donor earning $250,000, however, will receive an annual deduction of $75,000, a six-year aggregate tax deduction of $450,000, and an aggregate tax savings of $157,500.94

Pending Legislation

* Rural Heritage Conservation Extension Act of 2007 (S. 469)

In 2006, the president signed into law a bill increasing the charitable tax deduction for qualifying farmers and ranchers95 who donate property for a perpetual conservation easement from a maximum of 30 percent of adjusted gross income to 100 percent. It also raised the maximum deduction for other landowners donating land for easements from 30 percent to 50 percent and extended the period allowable to carry the tax deduction forward from five years to 15. The tax benefits expired December 31, 2007.96

But the Food and Energy Security Act of 2007 (the “farm bill” – pending when this report went to print) would extend the tax deduction increases for two years.97

* Endangered Species Recovery Act of 2007 (S. 700)

Sponsored by Senators Mike Crapo (R-Idaho) and Baucus, S. 700 would increase the tax benefits to property owners who donate land for conservation easements to the federal government. The easement can either be perpetual, 30-years, or a negotiated time limit. The bill would allow an income tax credit of 100 percent for perpetual conservation easements, 75 percent for 30-year easements, and 50 percent for negotiated limits. The bill is pending in the Senate Committee on Finance. Rep. Mike Thompson introduced the House companion bill H.R. 1422.98

Recommendations

1. Government should not be allowed to obtain conservation easements through prearranged acquisitions.

An easement acquired by a government agency through a public land trust does not require any approval process from either the public or the property owner and, therefore, is not accountable. Government agencies at any level of government should not be permitted to obtain land through preacquisitions or any form of arrangement with land trusts. If a landowner wishes to donate or sell an easement directly to a government entity, there is nothing preventing him from doing so.

2. No federal funding for nonprofit conservation groups.

Land trusts, through their definition as public charitable organizations, already benefit enormously by their federal tax-exempt status. Beyond this benefit, land trusts should work independent of tax-dollar handouts, which too easily can subject them to political pressures, coercion or influence from government. Government should end its use of subsidies, grants, and other funding to these nonprofit organizations.

3. Tax deductions should not require perpetuity.

A property owner has the right to do with his land as he wishes and should be entitled to place restrictions, if desired. However, given that changes in nature and science over time alter society’s definition of what is ecologically beneficial – and given the economic and ecological uncertainties of permanently encumbering land – government should not use tax dollars to effect perpetual conservation easements. Conservation easements differ from regular easements in that the “party” to be affected by the agreement is not one individual but the public as a whole. Future generations should not be burdened with inflexible, irreversible policies based on today’s land use decisions.

Specifically, conservation easements should be time-limited (“term easements,”) providing charitable income tax deductions to those individuals who restrict land use on their property in, say, 10- or 20-year increments.

Legislative language based on The Uniform Conservation Easement Act allows for easements limited in time as well as perpetual.99 Furthermore, a number of states provide tax incentives for term easements.100 California’s Williamson Act gives tax incentives to landowners who place agricultural easements on property for a minimum of 10 years under a “rolling contract” with local government.101 Other states such as North Dakota allow only term easements. Neither the federal nor state governments should be able to mandate perpetual terms as a condition of tax benefits.

4. Eliminate the estate tax.

It must first be said that the right to sell or donate one’s land or a portion of one’s land to a nonprofit organization or to a government entity is a property right. No matter what public policies are enacted governing conservation easements, individuals will always have the right to do with their property as they wish.

The issue is whether government through tax incentives should be able to influence property owners’ land use decisions, particularly considering problems with conservation easements outlined in this report.

While the overall objective of conservation easements is to discourage development, the rising burden of estate taxes on heirs is often the factor driving them to sell their property to developers. As Environmental Defense’s Michael Bean wrote back in 1997, the estate tax is “highly regressive in the sense that it encourages the destruction of ecologically important land in private ownership.”102 This is particularly true for farmers, whose annual income may pale compared to the value of the land. For the descendants of these land-rich, cash-poor landowners who simply do not have the resources to pay the taxes, their only option may be to sell the land to developers.103

Rather than attempting to patch up the problem by manipulating the tax code with tax breaks, a far more effective means of protecting land from development would be for federal and state governments to eliminate the “death tax” altogether.

As Jonathan Adler, a law professor at Case Western University, observes, “For too long policymakers have labored under the assumption that the only way to enhance environmental protection is the enactment of more federal rules and regulations. We forget that existing federal laws are often part of the problem.”104 A better alternative to tinkering with the tax code is to eliminate those policies that damage land preservation in the first place.

At the state level, 27 states – slightly more than half – impose an estate tax. Yet a number of these states, recognizing its damage on small, family farms, as well as its deterrence to retirees who otherwise might move to the state, are abolishing it. Virginia’s death tax expired in July 2007, Wisconsin’s in December 2007, and Kansas’ will end in 2009.105

5. Pending legislation.

The Food and Energy Security Act of 2007 (H.R.2419), Section 12203, would particularly benefit farmers and ranchers, who would receive a maximum 100 percent tax deduction on adjusted gross income for encumbering land via an easement. But rather than require perpetuity, landowner should be allowed to reconsider the conditions of the easement every 10 years. One way to handle the charitable income tax deduction would be to adjust the amount of the allowable tax benefit to correspond with the length of the term of the easement. In other changes, banning the transfer of a conservation easement from a land trust to a federal, state, or local government would ensure easements remain in private hands.

The Endangered Species Recovery Act of 2007 (S. 700) promotes government management and control of private lands and runs counter to the concept that easements work best operating under private ownership, private initiative, and private stewardship. Even zoning restrictions and takings require some degree of public approval and accountability. This bill would enable the government to control private property by appealing directly to land-rich, cash-poor landowners through generous tax credits.

Conclusion

What once showed promise as an effective tool for preserving lands through private ownership and stewardship is increasingly becoming a questionable practice, particularly as land trusts join government in partnerships and, in some cases, use conservation easements to turn private land over to government ownership. As the conservation easement and land trust movement continues to grow by leaps and bounds, it is imperative that reforms be put into place that return easements to their original intent to protect property through private means.

Requirements that easements encumber land in perpetuity remove one of the arrangement’s most significant benefits – flexibility. As the natural state of our environment and scientific discovery evolve, so do society’s definitions of what should be preserved and how. Tax policy should not lock future generations into relatively shortsighted visions of what today is considered ecologically-beneficial.

Finally, through manipulations to the tax code, government influences property owners’ decisions on land use, promising immediate tax relief to those who forfeit full rights and ownership of property. Were land trusts fully private organizations, free from government association and influence, there could be value. But given inherent problems with conservation easements, most pointed, the rise in government involvement, influence, and acquisition of lands under easement, a far more effective means would be to eliminate the estate taxes that discourage land preservation in the first place.

Dana Joel Gattuso is a senior fellow at the National Center for Public Policy Research.

Footnotes:

1 Also called a conservation covenant or servitude.

2 The focus of this paper is on conservation easements held by land trusts.

3 Under the federal tax code, the donor must agree to place the easement in perpetuity in order to receive tax benefits.

4 Exceptions are made in most cases for farming or ranching.

5 Federico Cheever and Nancy A. McLaughlin, “Why Environmental Lawyers Should Know (And Care) about Land Trusts and Their Private Land Conservation Transactions,” Environmental Law Reporter News & Analysis, Environmental Law Institute, Washington, D.C., March 2004, p. 10226.

6 Carol W. LaGrasse, “Conservation Easements: A Critical Commentary,” The Property Rights Foundation of America, Inc., March 14, 2000, at http://www.citizenreviewonline.org/feb_2002/conservation_easements_a_critical_commentary.htm.

7 Many, if not most, conservation easements are created to protect farming or ranching activities. Comments of Jean Hocker, President of the Land Trust Alliance, “What Makes for a Good Land Trust? A Roundtable Discussion,” Competitive Enterprise Institute, October 7, 1997.

8 Federico Cheever and Nancy A. McLaughlin, op. cit., p. 10226.

9 I.R.C. 170(h)(3) in Cheever and McLaughlin, op. cit., pp. 10225-6.

10 See Nancy A. McLaughlin, “Amending Perpetual Conservation Easements: A Case Study of the Myrtle Grove Controversy,” Abstract, University of Richmond Law Review, Vol. 40, p. 1031, at http://papers.ssrn.com/sol3/papers.cfm?abstract_id=903845. Also, Duncan M. Greene, “Dynamic Conservation Easements: Facing the Problem of Perpetuity in Land Conservation,” Seattle University Law Review, Vol. 28, No. 3, Spring 2005, p. 891, at http://papers.ssrn.com/sol3/papers.cfm?abstract_id=724281#PaperDownload.

11 Cheever and McLaughlin, op. cit., p. 10224.

12 See Sean Mulholland, “Land Trusts: The Growth of the Non-Profit Land Conservancy Movement,” Incentives and Conservation: The Next Generation of Environmentalists, ed. Daniel K. Benjamin, PERC (Bozeman, Montana), 2004, p. 8, at http://www.economicissues.net/papers/PERClandtrust.pdf.

13 They also differed from today’s conservation easement in that they were “appurtenant easements,” meaning the owner of the easement – in this case, the federal government – owned (bought up) land adjacent to the easement and, therefore, the arrangement was recognized under common law. See Mulholland, op. cit., p. 8. (More discussion on this under the section in this paper on common law.)

14 See Cheever and McLaughlin, op. cit., p. 10224-5. Also, see Mulholland, op. cit., pp. 9-12.

15 States needed to pass enabling legislation to allow conservation easements since the arrangements are not fully recognized under common law, which values active use of land rather than restrictions. See section “Are perpetual conservation easements inconsistent with common law?”

16 McLaughlin, “Conservation Easements – A Troubled Adolescence,” Journal of Land Resources & Environmental Law, Vol. 26, no. 1, p. 48, Note 2.

17 National Conference of Commissioners on Uniform State Laws, “Uniform Conservation Easement Act,” 1981, at http://www.cals.ncsu.edu/wq/lpn/PDFDocuments/uniform.pdf.

18 Land Trust Alliance in McLaughlin, “Conservation Easements – A Troubled Adolescence,” op. cit., pp. 49-50.

19 Land Trust Alliance, 2005 National Land Trust Census Report, November 30, 2006, p. 3-4, at http://www.lta.org/census/2005_report.pdf.

20 While the national membership organization for land trusts, the Land Trust Alliance, keeps track of data on conservation easements held by the nation’s local, state and regional land trusts, there is no source that carefully tracks the number of conservation easements held by the large national organizations. Also, see John Hart, “Private Land, Public Good: Taking Stock of Conservation Easements,” Bay Nature, Special Section: January-March 2006, at http://www.baynature.com/2006janmarch/easements_main.html.

21 Land Trust Alliance in McLaughlin, “Conservation Easements – A Troubled Adolescence,” op. cit., pp. 49-50.

22 Testimony of Steven J. McCormick, President and CEO of The Nature Conservancy, before the U.S. Senate Finance Committee, June 8, 2005; and Joseph M. Kiesecker, et. al., Conservation Easements in Context: A Quantitative Analysis of their Use by The Nature Conservancy,” Frontiers in Ecology and the Environment, Issue 3, Vol. 5, April 2007.

23 Land Trust Alliance, 2005 National Land Trust Census Report, op. cit., p. 15. Note: Dominic Parker maintains the portion of controlled land that trust groups hold in conservation easements is much higher – 78 percent in 2003 – than what the Land Trust Alliance reports because the Alliance counts “a handful of public agencies” it considers to be land trusts. See Dominic P. Parker, Conservation Easements: A Closer Look at Federal Tax Policy, PERC Policy Series, PERC, October 2005, pp. 6 & 24, at http://www.perc.org/perc.php?id=743.

24 McLaughlin, “Conservation Easements – A Troubled Adolescence,” op. cit., p. 51.

25 See Carol W. LaGrasse, op. cit..

26 See the Land Trust Alliance web site at www.lta.org. Also, Mulholland, op. cit.; and Parker, Conservation Easements: A Closer Look at Federal Tax Policy, op. cit., p. 6.

27 Ibid. Also, Mulholland, op. cit., p. 6.

28 See Cheever and McLaughlin, op. cit., p. 10232.

29 According to the Land Trust Alliance, the fastest increase in easement donations has occurred in states that provide the most generous state tax incentives. Land Trust Alliance, 2005 National Land Trust Census Report, op. cit., p. 8.

30 Rachel Emma Silverman, “Tax Break with a View,” The Wall Street Journal, February 7, 2007.

31 H.R.2419, Food and Energy Security Act of 2007, Section 12203.

32 See Cheever and McLaughlin, op. cit., p. 10225.

33 Parker, Conservation Easements: A Closer Look at Federal Tax Policy, op. cit., p. 9. Also, Land Trust Alliance, “State Tax Credits for Conservation,” Updated November 16, 2006, at http://www.lta.org/publicpolicy/state_tax_credits.htm.

34 Defenders of Wildlife, “State Government Incentives for Habitat Conservation: A Status Report,” March 2002, in Parker, op. cit., p. 9.

35 Study after study shows the failure of government as a steward of land. See Bruce Yandle, “Land Trusts or Land Agents?” PERC, December 1999, at http://www.perc.org/perc.php?id=375.

36 See Darla Guenzler, Ensuring the Promise of Conservation Easements, Bay Area Open Space Council, and Debra J. Pentz, Planning for Perpetuity: A Study of Colorado Conservation Easement Practices, Bay Conservation Resource Center (Boulder, Colorado), in Dominic P. Parker and Walter N. Thurman, “The Private and Public Economics of Land Trusts,” NC State Economist, NC State University, July/August 2004, p. 2, at http://www.ag-econ.ncsu.edu/VIRTUAL_LIBRARY/ECONOMIST/julyaug04.pdf.

37 Federico Cheever and Nancy A. McLaughlin, op. cit., p. 10233.

38 Julia D. Mahoney, Perpetual Restrictions on Land and the Problem of the Future, UVA Law & Economics Research Paper no. 01-6 and UVA School of Law, Public Law Research Paper no. 01-11, University of Virginia School of Law, December 2001, pp. 38, at http://papers.ssrn.com/sol3/papers.cfm?abstract_id=291537.

39 “Historical Origins of the Trustees of Reservations,” The Trustees of Reservations website, at http://www.thetrustees.org/pages/89_historical_origins.cfm.

40 Roger A. Cunningham, “Scenic Easements in the Highway Beautification Program,” 45 Denver Law Journal, 1968, pp. 182-3, in Nancy A. McLaughlin, “Increasing the Tax Incentives for Conservation Easement Donations: A Responsible Approach,” Ecology Law Quarterly, Vol. 31:1, pp. 102-3, supra note 405.

41 Ibid.

42 Mulholland, op. cit., p. 8.

43 See www.thetrustees.org.

44 See Congressional Testimony, Robert J. Smith, Adjunct Environmental Scholar, Competitive Enterprise Institute and Director of the Center for Private Conservation, before the Subcommittee on Parks, U.S. Senate Committee on Energy and Natural Resources, June 24, 2004, at http://energy.senate.gov/public/index.cfm?FuseAction=Hearings.Testimony&Hearing_ID=1243&Witness_ID=3629.

45 Thomas J. Bray, “Clear Thinking and Strategic Environmental Giving Are Making America More Beautiful,” Philanthropy Magazine, Jan.-Feb. 2004, at http://www.perc.org/articles/article448.php.

46 Ibid. Also, see the Sand County Foundation web site at http://www.sandcounty.net/foundation.

47 Bray, op. cit.

48 Michael De Alessi, “Can Land Trusts Be Trusted?” The American Enterprise Online, July 2000, at http://www.taemag.com/issues/articleID.17307/article_detail.asp.

49 See Sean Mulholland, op. cit., p. 13.

50 See Eve Endicott, “Preserving Natural Areas: The Nature Conservancy and Its Partners,” Land Conservation Through Public/Private Partnerships, ed. Eve Endicott, Lincoln Institute of Land Policy (Island Press: Washington, D.C. and Covelo, CA), 1993, p. 19.

51 Keith Wiebe, Abebayehu Tegene, Betsey Kuh, Partial Interests in Land: Policy Tools for Resource Use and Conservation, Introduction, Economic Research Service, U.S. Department of Agriculture, AER #744, November 1996, at http://www.ers.usda.gov/publications/AER744.

52 Yandle, op. cit.

53 De Alessi, op. cit.

54 Edward Thompson, Jr., “Preserving Farmland: The American Farmland Trust and Its Partners,” Land Conservation Through Public/Private Partnerships, op. cit., p. 47.

55 Lee Bumsted, “Partnerships Ensure Protection for Maine Lands,” Gulf of Maine Times, Vol. 7, No. 1, Spring 2003, at http://www.gulfofmaine.org/times/spring2003/mcht.htm.

56 U.S. Government Accountability Office, Report to the Subcommittee on Interior, Environment, and Related Agencies, Committee on Appropriations, House of Representatives, “Prairie Pothole Region,” GAO-07,1093, September 2007, p. 20 & 34, at http://www.gao.gov/new.items/d071093.pdf.

57 Ibid.

58 American Farmland Trust, Annual Report: 2006, p. 18; The Conservation Fund, Combined Financial Statements, Years Ended December 31, 2006 and 2005, p. 18; and The Nature Conservancy, Consolidated Financial Statements As of June 30, 2007 and 2006, p. 4.

59 U.S. Department of Agriculture, Forest Service, Forest Legacy Program National Report for Fiscal Year 2004, FS-816, December 2004, p. 2, at http://www.fs.fed.us/spf/coop/library/flp_nat_reprt_2004.pdf; Congressional Testimony, Dale Bosworth, Forest Service Chief, USDA Forest Service, before the Senate Finance Committee, March 4, 2005; and Congressional Testimony, Mark Rey, Undersecretary, USDA, before the Senate Energy and Natural Resources Committee, February 28, 2006. Dollars adjusted for inflation, using 2007 dollars.

60 Daniel Hellerstein, Cynthia Nickerson, et. al., Farmland Protection: The Role of Public Preferences for Rural Amenities, Economic Research Service, USDA, AER-815, November 2002. Dollars adjusted for inflation, using 2007 dollars.

61 See Julia D. Mahoney, op. cit.

62 Ibid, pp. 14, 19-22.

63 See Dana Joel Gattuso, “Forest Reforms in the Crossfire,” FoxNews.com, June 30, 2005, at http://www.foxnews.com/story/0,2933,160841,00.html.

64 Fred P. Bosselman & A. Dan Tarlock, The Influence of Ecological Science on American Law: An Introduction, 69 CHL-Kent L. Rev., 1994, pp. 847, 848, in Greene, op. cit., p. 907. See Greene, op. cit., p. 906.

65 See Greene, op. cit., p. 906.

66 Ibid, p. 915.

67 Ibid, p. 908.

68 See Pacific Legal Foundation in Christopher West Davies, “Pushing the Sprawl Back: Landowners Turn to Trusts,” New York Times, October 11, 2003.

69 Land Trust Alliance, 2005 National Land Trust Census Report, op. cit., p. 20.

70 See Timothy P. Duane, “Maximizing the Public Benefits of Agricultural Conservation Easements: A Case Study of the Central Valley Farmland Trust in the San Joaquin Valley,” University of California, Berkeley, June 12, 2006, at http://landscape.ced.berkeley.edu/~delta/classes/LA205/PublicBenefitsACEs.pdf. Also, Peter Fimrite, “Bay Area’s Open Space Tightrope,” San Francisco Chronicle, June 5, 2005.

71 Nancy A. McLaughlin, “Rethinking the Perpetual Nature of Conservation Easements,” Harvard Environmental Law Review, Vol. 29, Research Paper No. 05-03, 2005, p. 425, at http://www.law.harvard.edu/students/orgs/elr/vol29_2/mclaughlin.pdf.

72 Most land trusts make it clear to prospective grantors that a conservation easement will not likely be terminated and that “such changes are extremely rare and only occur where the amendment does not reduce the protection of conservation values.” See, for example, Vermont Land Trust, Conservation Easements: Guide to the Legal Document in Mahoney, p. 34.

73 UCEA Sec. 2 (a) & 3 (b), op. cit. Also, Cheever and McLaughlin, op. cit., p. 20131.

74 McLaughlin, “Rethinking the Perpetual Nature of Conservation Easements,” op. cit., p. 426. Also, see Cheever and McLaughlin, op. cit., p. 10231: “Relying on the vagaries of state law to resolve disputes regarding the modification and termination of perpetual easements may well prove to be difficult and costly.”

75 Mahoney, op. cit., p. 34.

76 See McLaughlin, “Amending Perpetual Conservation Easements: A Case Study of the Myrtle Grove Controversy,” op. cit., p. 1041.

77 Greene, op. cit., p. 904.

78 See McLaughlin, op. cit., p. 10231. Also, Greene, op. cit., p. 904.

79 Mahoney, op. cit., p. 43.

80 See Greene, op. cit., p. 891-2. Also, Mahoney, op. cit., p. 9.

81 Greene, op. cit., p. 892.

82 McLaughlin, “Conservation Easements – A Troubled Adolescence,” op. cit., p. 48, note 2.

83 Greene, op. cit., p. 893.

84 See James Burling in Pat Taylor, “Sacrificing Rights To Protect Property,” Insight on the News, May 13, 2002, Vol. 18, Issue 17. Also, Greene: “…neither [state] case law nor its statutory law eliminates the possibility that conservation easements will face common law challenges. However, practitioners can mitigate such risks by drafting the conservation easement with proper attention to common law and statutory requirements and to the perpetual nature of the easement.” Op. cit., p. 896. Note: A number of commentators on perpetual conservation easements have referred to the “rule against perpetuities” as a direct violation of common law. This is false. The rule refers to a limit under common law to when property is allowed to vest, that is to be transferred from the owner. It does not refer to how long one holds the property once the transfer takes place. See Melinda Harm Benson, “Perpetuity – What Does it Mean for Conservation Easements and the Wyoming Constitution?” November 2004, William D. Ruckelshaus Institute of Environment and Natural Resources, University of Wyoming, at http://www.uwyo.edu/OpenSpaces/docs/Perpetuities.pdf.

85 This section refers to “perpetual conservation easements,” since, in most cases, tax benefits are not available to grantors unless they are perpetual.

86 See Land Trust Alliance, 2005 National Land Trust Census Report, op. cit., p. 8.

87 Silverman, op. cit.

88 Stephen & Ottaway, “Developers Find Payoff in Preservation: Donors Reap Tax Incentive by Giving to Land Trusts, but Critics Fear Abuse of System,” Washington Post, December 21, 2003.

89 See Joe Stephens & David B. Ottaway, “Nonprofit Sells Scenic Acreage to Allies at a Loss: Buyers Gain Tax Breaks with Few Curbs on Land Use,” Washington Post, May 6, 2003. Also, Stephens & Ottaway, “Developers Find Payoff,” op. cit.

90 Joint Committee on Taxation, Options To Improve Tax Compliance and Reform Tax Expenditures, Prepared by the Staff of the Joint Committee on Taxation, #JCS-02-05, January 27, 2005, pp. 281, 284 & 427, at http://www.house.gov/jct/s-2-05.pdf.

91 Ibid, p. 285.

92 See the Land Trust Alliance, “Land Trust Standards and Practices,” last updated July 23, 2007, at http://www.lta.org/sp/. Also, Joe Stephens, “Alliance Starts Plan to Improve Land Trusts,” Washington Post, April 20, 2005, p. A08; and Joe Stephens and David B. Ottaway, “Senators Question Conservancy’s Practices,” Washington Post, June 8, 2005, p. A03.

93 Silverman, op. cit.

94 The example assumes a charitable tax deduction capped at 30 percent. See McLaughlin, “Increasing the Tax Incentives for Conservation Easement Donations: A Responsible Approach,” op. cit., p. 32.

95 Defined as individuals who earn at least half their annual income from farming or ranching. Public Law 109-280, Section 1202.

96 Ibid.

97 H.R.2419, Food and Energy Security Act of 2007, Section 12203. See Library of Congress, Thomas, at http://thomas.loc.gov/.

98 Ibid.

99 National Conference of Commissioners on Uniform State Laws, “Uniform Conservation Easement Act: Summary,” at http://www.nccusl.org/nccusl/uniformact_summaries/uniformacts-s-ucea.asp.

100 Anita M. Zurbrugg, Less-than-perpetuity and Agricultural Conservation Easements, American Farmland Trust, Center for Agriculture in the Environment, April 14, 2003, p. 15.

101 See The California Land Conservation (Williamson) Act: Status Report, 2006, p. 1, at http://www.consrv.ca.gov/DLRP/lca/pubs/status%20reports/2006/Williamson%20Act%20

Status%20Report%202006%20(complete).pdf.

102 Michael J. Bean, “Shelter from the Storm,” The New Democrat, April 1997.

103 See Jonathan H. Adler, “The Anti-Environment Estate Tax: Why the ‘Death Tax’ Is Deadly for Endangered Species,” Competitive Enterprise Institute, On Point, No. 35, April 20, 1999.

104 Ibid. Also, see “Living on Earth,” Public Radio International, Estate Tax Battle, June 7, 2002, at http://www.loe.org/shows/shows.htm?programID=02-P13-00023#feature6.

105 Ashlea Ebeling, “Tax-free in the Rust Belt,” Forbes, August 13, 2007.