01 Aug 2013 Why The “Young Invincibles” Won’t Participate In The ObamaCare Exchanges and Why It Matters

Executive Summary

If the ObamaCare health insurance exchanges are to function properly, it is crucial that a substantial number of people ages 18-34 join them. This age group that is young and relatively healthy must purchase health insurance on the exchanges in order to “cross-subsidize” people who are older and sicker. Without the young and healthy, the exchanges will enter a “death spiral” where only the older and sicker participate and price of insurance premiums will increase precipitously.

This study finds that in 2014 many single people aged 18-34 who do not have children will have a substantial financial incentive to forgo insurance on the exchanges and instead pay the individual mandate penalty of $95 or one percent of income. About 3.7 million of those ages 18-34 will be at least $500 better off if they forgo insurance and pay the penalty. More than 3 million will be $1,000 better off if they go the same route. This raises the likelihood that an insufficient number of young and healthy people will participate in the exchanges, thereby leading to a death spiral.

Introduction

Haley Townsend is a pleasant 22-year-old woman working at a shop in Washington, D.C.’s Union Station. Like many her age, she is uninsured.

While she sees some value in insurance, she claims she doesn’t need it right now.

“Overall, I’m pretty healthy,” she said. “The only thing I need to see the doctor about are the glasses I wear.”

Haley currently earns about $18,100 annually. She’s also going through divorce proceedings that have put her into considerable debt.

“Right now, a lot of my paycheck goes toward paying that off,” she said. Thus, financially she has little room for error and no room to pick up a major new expense like health insurance. Yet due to ObamaCare, in 2014 Haley is expected to purchase health insurance through the Washington D.C. “exchange”—known as the Health Benefit Exchange Authority—or pay a fine of $95.

If Haley buys health insurance through Washington D.C.’s exchange, she’ll be eligible for a subsidy of about $1,329 under ObamaCare to help her pay for insurance. If she puts that toward the lowest-cost Bronze plan on the exchange, about $1,541, then she’ll only have to pay about $212 out-of-pocket for health insurance.

That may not seem like much, but for Haley that $212 represents about 14 percent of one of her monthly paychecks before taxes. If she instead pays the $95 fine, then she’ll save $117. “I could easily use that money for groceries or transportation,” she said.

Clearly, Haley has a financial incentive to forgo insurance next year, the first year that the exchanges and the individual mandate go into effect. However, she is exactly the type of young and healthy person that the exchanges must attract.

Those aged 18-34, sometimes called the “young invincibles,” tend to be healthier and use less medical care among the age cohorts eligible to participate on the exchanges. Among those aged 18-34, only about 2.7 percent rate themselves in fair or poor health. By contrast, 5.3 percent of those aged 35-50 and 9.6 percent of those aged 51-64 rate themselves in fair to poor health. Those aged 18-34 average about 2.7 physician visits per year while those aged 35-50 average about 3.3 and those aged 51-64 average about 4.8.1 The only way to keep the health insurance premiums on the exchanges relatively low is if enough 18-34-year-olds participate in them. A sufficient number of young and healthy people must buy insurance through the exchanges to help “cross-subsidize” those people who are older and sicker.

Yet millions of individuals will have an even greater financial incentive than Haley does to decline purchasing insurance on the exchanges. Indeed, this study finds that over 3.7 million single individuals aged 18-34 without children will save at least $500 by declining insurance and paying the fine in 2014. Over 3 million individuals will save at least $1,000. That makes it unlikely that the exchanges will be able to offer affordable health insurance in the long run.

The Exchanges

Under ObamaCare, an exchange is an online marketplace for purchasing insurance set up either by state governments or the federal government. According to the Kaiser Family Foundation, 16 states and Washington, D.C are setting up their own exchanges, 27 states have decided to let the federal government run their exchange, and seven states are setting up a “hybrid” exchange in which the state and federal government share authority.2 Insurance plans on the exchanges will be listed as either Platinum, Gold, Silver or Bronze, depending on how much of a person’s medical expenses they cover. Platinum plans will cover the most and, hence, will be the most expensive plans. On the other end, Bronze plans cover the least and will be the cheapest.3

Exchanges use both “community rating” and “guaranteed issue,” two regulations that, as explained below, incentivize the young and healthy to avoid buying insurance.

To compel the young and healthy to purchase insurance, the architects of ObamaCare included an individual mandate that requires individuals to either buy insurance or pay a penalty. The penalty, which increases over time, is whichever is greater: $95 or one percent of income in 2014, $325 or two percent of income in 2015, and $695 or 2.5 percent of income in 2016 and thereafter.

When arguing before the United States Supreme Court in defense of the individual mandate, the Obama Administration Solicitor General Donald Verrilli explained that the mandate is vital to keeping insurance premiums on the exchange affordable:

Congress understood that [without the mandate] healthy individuals have an incentive to stay out until their need for insurance arises while, at the same time, those with the most serious immediate health care needs have a strong incentive to obtain coverage. Premiums would therefore go up, further impeding entry into the market by those currently without acute medical needs.4

The architects of ObamaCare also provided subsidies for the purchase of insurance on the exchanges to encourage people such as Haley to buy it. The subsidies are available to those with incomes between 100 percent and 400 percent of the federal poverty level (FPL) in states that have not expanded Medicaid and 138 percent to 400 percent FPL for those in those states that have expanded Medicaid. The subsidies work on a sliding scale, with the largest going to those earning near 100 or 138 percent FPL. The amount of the subsidy diminishes until one’s income reaches 400 percent FPL, above which no subsidy is available.

The New Republic’s Jonathan Cohn, an able defender of ObamaCare, calls the subsidies essential for making the exchanges work. If subsidies are not provided on the exchanges, he argues, the “real world effect… would be to deprive residents of these states of financial assistance and access to affordable insurance.”5

Yet the individual mandate and the subsidies will not be sufficient to induce adequate numbers of the young and healthy to participate in the exchanges. Rather, these individuals will have considerable incentive to forgo insurance until they are older and sicker, thereby sending the exchanges into an insurance “death spiral.”

What Else Can One Buy With $1,000?

This study employed the exchange subsidy calculator of the Kaiser Family Foundation and U.S. Census Bureau data. The Silver and Bronze premiums in the Kaiser Family Foundation calculator are based on estimates from the Congressional Budget Office. Exchange premiums released in a few states are on average 18 percent less than the Congressional Budget Office estimate.6 Thus, the premiums from the Kaiser Family Foundation calculator were reduced 18 percent for this study.

The subsidy calculators were then used to determine the income at which the out-of-pocket cost for a Bronze-level plan for a single individual age 18-34 without children would be at least $500 above the 2014 fine of $95 or one percent of income and the income at which the out-of-pocket cost would be at least $1,000 above the 2014 fine. Then Census Bureau data was used to determine how many people had incomes at and above those levels. Census Bureau data was also used to determine which individuals were either uninsured or had private insurance not purchased through an employer and therefore were most likely eligible to purchase insurance from an exchange. (For a more detailed description of the methods, see the section on methodology at the end.)

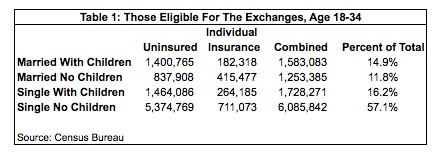

Participation of single adults without children will be crucial if the exchanges are to succeed because they form the largest group of those ages 18-34. Table 1 shows the breakdown of those who are most likely to be eligible for the exchanges:

Of those ages 18-34, those who are uninsured or have insurance through the individual market comprise over 57 percent of the group most likely to be eligible for the exchanges. The Congressional Budget Office Estimates that seven million people will participate in the exchanges in 2014.7 But will enough of the 18-34 age group join?

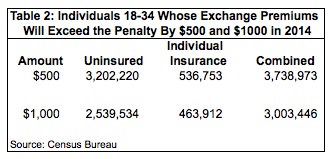

To answer that question, this study examines the out-of-pocket costs that these individuals would pay for a Bronze insurance premium on the exchange. Table 2 shows the results:

Over 3.7 million individuals will pay at least $595 out-of-pocket for a Bronze plan, meaning that they will save at least $500 if they decline insurance and pay the fine. About 3 million individuals will save at least $1,000 if they go the same route.

In both cases the uninsured comprise the bulk of these individuals. These people have already decided, for whatever reason, that purchasing insurance is not worth the cost. Getting these people to shell out $500 or $1,000 of their own after-tax income is going to be a difficult task, to say the least.

Also noteworthy is that a large portion of the total number of single people without children ages 18-34 have a substantial financial incentive not to participate next year. Sixty-one percent will have at least $500 worth of incentive to avoid the exchange, and 49 percent will have at least $1,000 worth.

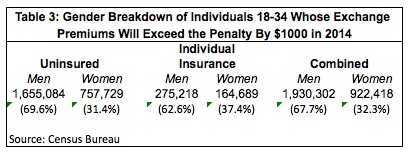

The gender breakdown of these individuals presents another problem. Women have higher rates of health utilization than men, including more visits to primary-care physicians and greater use of diagnostic tests and emergency care.8 However, as Table 3 shows, roughly two-thirds of the individuals for whom insurance will cost at least $1,000 more than the fine are men.

To avoid a death spiral of rising costs and falling participation, the exchanges must attract many people who are the least likely to make medical claims so they can cross-subsidize those with large medical claims. Yet those most likely to have small claims amounts—men—comprise a much larger percentage of those with substantial financial incentive to avoid the exchanges.

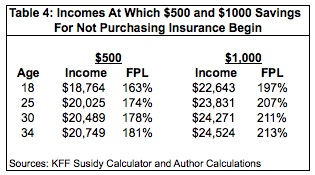

The analysis also finds that, in 2014, those with an incentive to pay the fine instead of purchase insurance begin at the lower end of the income scale. A Milliman analysis on the strength of the individual mandate shows that, in 2016, when the penalty rises to $695 or 2.5 percent of income, the incentive to pay the penalty instead of buying insurance doesn’t grow until one’s income gets closer to 300 percent FPL, or $34,470 for an individual.9 As Table 3 shows, this study finds for an 18-year-old the $500 incentive to decline insurance and pay the penalty begins at 163 percent FPL and begins at 181 percent for a 34-year-old. The $1,000 incentive to pay the fine begins at 197 percent FPL for an 18-year-old and at 213 percent FPL for a 34-year-old.

For those at or near the incomes listed in Table 4, $500 and $1,000 is a considerable amount of money.

While many young and healthy Americans no doubt value health insurance, it competes with many other things they value, many of which are, arguably, of considerable importance in their lives. For example, consider what a 25-year-old could use the money for if he declines insurance. If he makes $20,025, the $500 he’ll save by not purchasing insurance could easily be one month’s rent for many apartments in the U.S.

At $23,831 annual income, that 25-year-old will save $1,000 by just paying the one percent fine. That’s a savings of about $83 a month that can purchase a month’s worth of groceries for a single person at a grocery store such as Aldi.10

Additionally, some individuals may avoid buying insurance because of values that are less tangible but no less important. “I don’t like the fact that I’m required to buy insurance if I think I don’t need it,” said Haley. “I should have that freedom. It should be my choice.”

The “Death Spiral”

If the exchanges do not attract a sufficient number of people in the 18-34 age demographic, they will eventually enter an insurance “death spiral.” This occurs when the young and healthy drop out of the “insurance pool.” This leads to “adverse selection” in which insurance is only attractive to those who are generally older and sicker. If the insurance pool is comprised largely of people who are older and sicker, then insurance prices will rise to cover their costs. That rate increase causes even more young and healthy people drop their insurance, leaving the pools even older and sicker than before, and so on. Eventually, all but a few insurers will be forced to discontinue their business on the exchanges because they can no longer make a profit. Fewer insurers means less competition, resulting in even higher insurance premiums.

Community rating and guaranteed issue are catalysts for a death spiral. In its strictest form, community rating means that insurers must charge everyone the same premium, regardless of factors such as health status and age. Guaranteed issue means that an insurer must sell a policy to a consumer anytime.

Under ObamaCare, the exchanges use a modified version of both of these regulations. Its form of community rating doesn’t allow insurers to vary rates based on health status. It does allow, however, for modification of premiums if one smokes and to compensate for age (although in a more restricted manner than the market currently does). Regarding guaranteed issue, insurers must sell policies to all comers but (with a few exceptions) only during the annual open enrollment period from October to December.

Both of these rules give young and healthy people big incentives to forgo insurance coverage altogether. Community rating means young people have a reduced incentive to buy insurance since they will pay a premium that is above the market rate. Many who are currently purchasing insurance in the individual market, for example, will see a substantial premium increase if they switch to the exchange.11

In a market without guaranteed issue, consumers run the risk of insurers not selling them policies when they get seriously ill. But that risk is largely gone under the exchanges. For instance, a young person who gets a serious illness in June only has to wait until October to sign up for insurance and then wait until January 1 of the next year to receive coverage. Combined, community rating and guaranteed issue give the young and healthy big incentives to forgo insurance until they are sick.

The late Conrad Meier, then a senior fellow in health care policy for the Heartland Institute, examined what happened when these two regulations were instituted on the state level in his 2005 monograph “Destroying Insurance Markets.” In the early 1990s eight states — Kentucky, Maine, Massachusetts, New Hampshire, New Jersey, New York, Vermont and Washington — imposed community rating and guaranteed issue on their individual insurance markets. The result, according to Meier, was the above-described death spiral.

For example, in 1992 the New Jersey legislature adopted community rating and guaranteed issue rules for its individual insurance market with the passage of the “Individual Health Coverage Program.” The monthly premium for family coverage from Aetna rose from $769 in 1994 to $6,005 in 2005, a whopping increase of 683 percent! Other insurers saw similar increases.12

Before the reforms began, there were about 28 insurers covering the New Jersey individual market.13 By 2007 there were only seven.14 According to the Census Bureau, the number of people in New Jersey’s individual market fell from about 998,000 in 1994 to 630,000 in 2005, a decline of 37 percent.15

As noted above, the architects of ObamaCare attempted to avoid this kind of disaster with an individual mandate and premium subsidies. But with millions of young, healthy individuals having considerable financial incentive to pay the penalty instead of buying insurance, it is likely that the mandate and subsidies will also prove insufficient.

Discussion

The Obama Administration estimates that it will need about 2.7 million 18-30-year-olds to join the exchanges next year if the exchanges are to work.16 While this study examined those aged 18-34, a quick run of the data shows that there are about 4.3 million 18-30-year-old single individuals who would be eligible for the exchanges. Of those about 2.9 million have a $500 incentive to avoid the exchange and about 2.38 million have a $1,000 incentive. Even if we assume that those who do not buy insurance are limited to those with the $1,000 incentive, the exchanges would still come up about 780,000 short of the 2.7 million 18-30-year-olds needed to avoid a death spiral.

Some recent developments, such as the Obama Administration’s decision to suspend the employer mandate for at least a year, may change the incentives for some younger people facing the prospect of insurance on the exchange. Both Grace-Marie Turner of the Galen Institute and Douglas Hotlz-Eakin of the American Action Forum argue that suspension of the employer mandate gives employers a big incentive to push their employees into the exchanges. Employers can lower their costs by reducing or eliminating their health insurance expenses, while employees can get subsidized coverage on the exchange. Holtz-Eakin said “Obama Administration officials have just created ‘one of the broadest and deepest advertising networks’ they could have imagined to spur enrollment in the ObamaCare exchanges” since employers have direct lines of communication with their employees.17

While that’s a very plausible scenario, the lingering question is whether or not the young and healthy who are dropped from employer-based coverage will be eager to join the exchanges.

First, people working for firms that provide insurance often have minimal out-of-pocket premium costs. Such workers would be moving to the exchange where they could very well have substantial out-of-pocket premium costs that incentivize them to forgo insurance and pay the penalty. Further, some young employees already decline their employer-based insurance. Firms with more than 35 percent of their workers age 26 or less have a an average take-up rate of health insurance of 60 percent, while there is a 79 percent take-up rate at firms with less than 35 percent of workers under age 26.18 Thus, it’s not safe to assume that employers dropping coverage will create a prime source of young and healthy customers for the exchanges.

Another reason young and healthy Americans might sign up with the exchanges is that they may be able to get subsidies they don’t qualify for by reporting an income lower than what they actually earn. The Obama Administration has said that it will be unable to verify an individual’s or family’s income via the exchanges for 2014, so it will instead rely on an “honor system.”19

However, as Robert Book of the Heritage Foundation has noted, the Obama Administration has suspended more than just the employer mandate. The provisions that contain the employer mandate also contain requirements that employers and insurers report employees’ insurance information. Those requirements are suspended too, and without such information it will be next to impossible for the federal government to enforce the individual mandate.20 Thus, the young and healthy can even possibly avoid paying the $95 penalty as well.

While some may be tempted to lie about their income to qualify for subsidies, they will have to pay those subsidies back when they report their 2014 income on their tax return.21 Whether they will have to do the same with the individual mandate penalty is unclear, but — for this scenario — assume they will. In this case, they will face a choice between paying back hundreds if not thousands of dollars in subsidies or a fine of $95 or one percent of income. With that set of incentives, expect the young and healthy to be more likely to forgo insurance, thereby triggering a death spiral.

Finally, this analysis suggests that many people who currently get insurance through the individual market may drop coverage when confronted with purchasing it through an exchange. The irony is that one of the purported goals of ObamaCare was to reduce the amount of people who are uninsured. The exchanges, though, may only increase their number.

Methodology

1. The first step in this study was using the Kaiser Family Foundation (KFF) subsidy calculator to create an Excel file with all of the income data necessary to calculate premiums. Once that was done, the premiums in the KFF calculator were reduced 18 percent. So, for example, the Silver and Bronze premiums for a 21-year-old in the KFF calculator are $3,018 and $2,501, respectively. Reducing those 18 percent yields premiums of $2,475 and $2,051 , respectively. The Excel file was then used to determine the premium costs for the rest of the 18-34 age range and the lowest income at each age level at which the out-of-pocket costs for the Bronze premiums were either $595 and $1,095, or $500 and $1,000 plus the fine of 1 percent of income. The KFF calculator was used to double-check those results.

2. The second step was determining the highest income at each age level at which the individual mandate penalty when applied to the premium would equal less than $500 and $1,000. This was done because in 2014 the penalty is whichever is greater, $95 or 1% of income. To determine this, both $500 and $1,000 were subtracted from the full price of the Bronze premium. For someone age 21 the full price of the Bronze premium is $2,051. Subtracting $500 equals $1,551 and $1,000 equals $1,051. Then $1,551 and $1,051 would be divided by 1% to get the top income at which the out-of-pocket cost for the Bronze premium would still be $500 and $1,000 after subtracting the fine. For someone age 21, those top incomes were $155,100 for $500 and $105,100 for $1,000.

One more step was involved, as the percentage will be applied to income after the personal exemption and standard deduction are subtracted on an individual’s taxes. The personal exemption is currently $3,900 and the standard deduction is $6,100, for a total of $10,000. Thus, $10,000 was added to each top income. So, for someone age 21, the top incomes would be $165,100 and $115,100, respectively.

3. To calculate how many single, childless individuals fell within each income range for each age, the study used the U.S. Census Bureau’s Current Population Survey, March 2012 Supplement.

The variables used included:

A_AGE – age

PTOTVAL –person’s total income

A_MARITL – person’s marital status

FOWNU18 – number of children under 18

HI_YN – Have private health insurance

HIOWN – Health insurance is in own name

HIEMP – Health insurance offered through employer

Most of the variables are self-explanatory with the exception of the health insurance variable. The variable for having private insurance gave three options: yes, no, and “not in universe.” “Not in universe” was excluded from that variable as that would include anyone with a public form of insurance, such as Medicare or Medicaid. Next, HIOWN was used to exclude those age 26 and under who would have insurance through their parents’ policy. Finally, HIEMP was used to exclude those who had private insurance through their employers. What remains should be those who have insurance through the individual market or are uninsured.

David Hogberg, Ph. D., is a health care policy analyst for the National Center for Public Policy Research.

Footnotes:

1 U.S. Census Bureau, Survey of Income and Program Participation.

2 The Henry J. Kaiser Family Foundation, “State Decisions For Creating Health Insurance Exchanges, as of May 28, 2013,” at http://kff.org/health-reform/state-indicator/health-insurance-exchanges/ (July 10, 2013).

3 The exchanges will also offer a cheaper “Catastrophic Plan.” However, it will be primarily available to those ages 18-29 and no subsidies will be available for them.

4 Brief For Respondents, National Federation of Independent Business, Et Al., Petitioners v. Kathleen Sebelius, Secretary of Health and Human Services, Et Al; State of Florida, Et Al., Petitioners, v. Department of Health and Human Services, et al., Nos. 11-393 and 11-400 (Supreme Court, May 26, 2012), pp. 46-47.

5 Jonathan Cohn, “ObamaCare’s Critics Refuse to Give Up,” The New Republic, November 20, 2102, at http://www.newrepublic.com/blog/plank/110322/obamacare-oklahoma-lawsuit-federal-exchange-subsidies-cannon (May 2, 2013).

6 Laura Skopec and Richard Kronick, “Market Competition Works: Proposed Silver Premiums in the 2014 Individual and Small Group Markets Are Nearly 20% Lower than Expected,” ASPE Issue Brief, Department of Health and Human Services, July 2013, at http://aspe.hhs.gov/health/reports/2013/MarketCompetitionPremiums/rb_premiums.pdf (July 18, 2013).

7 Congressional Budget Office, “CBO’s February 2013 Estimate of the Effects of the Affordable Care Act on Health Insurance Coverage,” at http://www.cbo.gov/sites/default/files/cbofiles/attachments/43900_ACAInsuranceCoverageEffects.pdf (May 7, 2013).

8 Klea D. Bertakis, Rahman Azari, L. Jay Helms, Edward J. Callahan, and John A. Robbins, “Gender Differences in the Utilization of Health Care Services,” Journal of Family Practice, February 2000, Vol. 49, No. 2; and Klea D. Bertakis and Rahman Azari, “Patient Gender Difference in the Prediction of Medical Expenditures,” Journal of Women’s Health, October 2010, Vol. 19, No. 10.

9 Paul R. Houchens, “Measuring the Strength of the Individual Mandate,” Milliman Research Report, Milliman, March 2012.

10 At www.aldi.us one can find two packages of Oscar Meyer Ham for $7.98, two packages of Lunchmate Turkey for $5.98, two packages of Parkview Hot Dogs for $1.50, 10 packages of shells and cheese for $12.90, 1 container of peanut butter for $1.89, and two packages of hot dog buns for $1.78. The total comes to $32.03, leaving over $50 for milk, cereal, fruits, vegetables and sales tax.

11 Louise Radnofsky, “Health-Insurance Costs Set For A Jolt,” Wall Street Journal, June 30, 2013, at http://online.wsj.com/article/SB10001424127887324251504578577760224985382.html (July 2, 2013).

12 Conrad F. Meier, “Destroying Insurance Markets: How Guaranteed Issue and Community Rating Destroyed the Individual Health Insurance Market in Eight States,” Council for Affordable Health Insurance and The Heartland Institute, 2005, at http://www.cahi.org/cahi_contents/resources/pdf/destroyinginsmrkts05.pdf (May 3, 2013).

13 Meier, 2005.

14 Leigh Wachenheim and Hans Leida, “The Impact of Guaranteed Issue and Community Rating Reforms on Individual Insurance Markets,” Milliman, August 2007, p. 25.

15 U.S. Census Bureau, “Historical Health Insurance Tables, Table HI-4,” at http://www.census.gov/hhes/www/hlthins/data/historical/orghihistt4.html (July 10, 2013).

16 Matthew Yglesias, “Obamacare Skeptics Are Deluding Themselves,” Slate, July 16, 2013, at http://www.slate.com/articles/business/moneybox/2013/07/

obamacare_implementation_fight_the_white_house_has_a_plan_and_it_s_going.html (July 18, 2013).

17 Grace-Marie Turner, “ObamaCare’s Costs Are Set To Soar As Administration Encourages Companies To Drop Health Benefits,” Galen Institute, July 15, 2013, at http://www.galen.org/newsletters/obamacares-costs-are-set-to-soar-as-administration-encourages-companies-to-drop-health-benefits/ (July 15, 2013).

18 The Henry J. Kaiser Family Foundation, “2012 Employer Health Benefits Survey,” September 11, 2012, p. 52.

19 Sarah Kliff and Sandhya Somashekhar, “Health insurance marketplaces will not be required to verify consumer claims,” Washington Post, July 5, 2013, at http://www.washingtonpost.com/national/health-science/health-insurance-marketplaces-will-not-be-required-to-verify-consumer-claims/2013/07/05/d2a171f4-e5ab-11e2-aef3-339619eab080_story.html (July 6, 2013).

20 Robert Book, “By Delaying Obamacare’s Employer Mandate, Did The White House Also Delay The Individual Mandate?” The Apothecary, Forbes, July 8, 2013, at http://www.forbes.com/sites/theapothecary/2013/07/08/did-they-postpone-the-individual-mandate-also/ (July 14, 2013).

21 Kliff and Somshekhar, 2013.