14 Sep 2014 Despite ObamaCare Supporters’ Claims, Health Insurance Plans Prior to ObamaCare Exchanges Were Neither “Crappy” Nor “Substandard”

Executive Summary

When millions of people in the individual health insurance market lost their health plans in late 2013, ObamaCare supporters claimed those lost plans were “substandard” or “crappy.” However, they failed to support that contention.

This study examines the claim that the policies on the individual market were inferior in quality to those on the ObamaCare exchanges. First, it compares the premiums and the size of the deductibles as well as maximum out-of-pocket costs of policies on the individual market prior to the exchanges to those of current polices on the exchanges. Second, it examines the quality of provider networks by comparing the number of plans that are HMOs versus those that are PPOs in the individual market prior to the exchanges and those now on the exchanges.

The study finds that there were many policies on the individual market that had lower premiums and lower or equal deductibles and out-of-pocket maximums than the cheapest plans now available on the exchanges. It also finds that the individual market prior to the exchanges offered a greater choice of hospitals and physicians since it contained far more PPO policies than HMO policies, whereas the exchanges offer more HMO policies.

Introduction

ObamaCare supporters have repeatedly denigrated health insurance policies that do not meet ObamaCare standards. They used the “substandard” excuse to explain why millions of people in the individual market received notices cancelling their plans in the last months of 2013.

In late October 2013, President Obama said:

Now, if you had one of these substandard plans before the Affordable Care Act became law and you really liked that plan, you’re able to keep it. That’s what I said when I was running for office. That was part of the promise we made. But ever since the law was passed, if insurers decided to downgrade or cancel these substandard plans, what we said under the law is you’ve got to replace them with quality, comprehensive coverage — because that, too, was a central premise of the Affordable Care Act from the very beginning.1

Ed Schultz, host of MSNBC’s “The Ed Show,” dismissed the concerns of people who had lost their plans, saying: “Some of them are gonna get these [cancellation] notices because… they have crappy insurance.”2

In November 2013, President Obama issued an executive order allowing people who had received a cancellation notice to keep their plans. This did not sit well with some liberal lawmakers, such as Iowa Senator Tom Harkin, who said he was “concerned about people having policies which don’t do anything. They’re just junk policies.”3

Substandard, junk, crappy: ObamaCare proponents assumed that plans on the individual market prior to the exchanges were inferior to those on the exchanges. However, they failed to support that claim. This study puts the proponents’ claim to the test. It examines plans currently on the exchanges and compares them with those plans that were available through eHealthinsurance.com (eHealth) and Finder.healthcare.gov (Finder) in 2013 in ten metropolitan areas for a single 27-year-old and a 57-year-old couple. It then compares the plans on two aspects of quality.

This study first examines the premiums, deductibles and out-of-pocket maximums of the plans. A deductible is the amount that the policyholder has to pay before the insurance company begins partially paying for benefits. The out-of-pocket-maximum (OOPM) is the amount the policyholder must pay before the insurer begins paying for 100 percent of benefits. This study examines the plan with the cheapest premium on the exchanges for each of four levels: catastrophic, bronze, silver and gold. It then examines eHealth and Finder to determine if there were plans available that had both lower premiums and lower or equal deductibles and OOPMs than the cheapest plan on the exchanges.

Second, it compares the networks of physicians and hospitals in the plans on the exchanges to those on eHealth and Finder and examines whether the exchanges or eHealth and Finder offer more plans with less restrictive networks.

Pam Hopmann

Pam Hopmann, age 63, lives in Chesterfield, Missouri. Her experiences are a microcosm of the problems caused by ObamaCare in the last year. She lost her insurance and purchased an exchange policy that has both higher premiums and out-of-pocket-costs and does not cover her physicians.

For years, Pam was covered under her husband’s employer-based plan. When he retired, she stayed on his plan for an additional 18 months via a federal law known as “COBRA.” That ran out in January of 2013.

When she looked for coverage on the individual market, she was unable to get a policy because of a congenital heart condition.

“It’s ironic, because the last ten years I’ve had some health problems, but that’s not really one of them,” she said. “In fact, I only found out about my condition a few years ago.”

She was able to get coverage through the temporary Pre-Existing Condition Insurance Plan (PCIP) created under ObamaCare for people who are high risk. She paid about $400 a month in premiums and had a $1,000 deductible, which she found reasonable.

“Another reason I was very happy with it was most of my doctors were in the network of this plan,” she said. “I’ve been seeing my ob/gyn [obstetrician and gynecologist] for about 30 years and he was on the plan through my husband’s work and then on the PCIP plan.”

But in September of 2013, she received a notice that her PCIP plan would be cancelled at the end of the year.

“My husband and I started trying to sign up for insurance on the exchange, but we never got through,” she said. “We ended up using an insurance agent.”

She ended up choosing a gold plan, a “$10 Copay PPO” policy from Coventry Health Care. She qualifies for a monthly subsidy, but even with that she is still paying a higher premium of $544 a month. She also has a higher deductible of $1,750.

That deductible, however, is limited to the physicians who are in the plan’s network. For out-of-network physicians, the plan has a much higher $5,000 deductible.

“In the fall of 2013 I started receiving letters from my physicians, including my ob/gyn and cardiologist, saying that they wouldn’t be taking insurance on the exchange because the reimbursement rates were too low,” Pam said. “Now I have to pay full price to see my doctors where before I had just a 20 percent copay.”

Overall, she thinks her new plan is inferior.

“The bottom line is it’s costing me more, my doctors aren’t in network, and I’m not sure it gives me any new benefits.

“I just really feel like it was shoved down our throats — like I had no choice,” Pam said. “Obama said we could keep our plans and keep our doctors, and I couldn’t do either of those. I think that’s wrong because if you had something you liked, you should have been able to stick with it.”

Quality

From an economic perspective, “quality” means that “characteristic of a product or service that satisfies the customer’s wants and needs in exchange for monetary considerations.”4 There is obviously a great deal of subjectivity inherent in the concept of quality. For example, some customers may think that an insurance policy that costs $150 per month that has a $1,000 deductible is good value for the money. Others may see it as a bad deal.

However, there is one aspect of quality regarding health insurance that is rather objective: the relationship of the premium to the deductible and OOPM. Specifically, few people, if any, would consider it good value for the money to change to a policy with a higher premium and a higher deductible and OOPM than a policy they previously owned. In other words, looking solely at the aspect of premium relative to out-of-pocket costs, almost no one would rationally consider it an improvement in quality to pay a higher premium and get less out-of-pocket coverage.

This became a very real problem as the ObamaCare exchanges became more functional in late 2013. As one news account noted, “many people with modest incomes are encountering a troubling element of the federal health law: deductibles so steep they may not be able to afford the portion of medical expenses that insurance doesn’t cover.”5 A Health Pocket study found that deductibles for bronze plans were, on average, 42 percent higher than plans that were on the individual market in 2013.6 Typical were stories like that of Adam Weldzius, who would have seen his deductible triple if he wanted an exchange plan that had a premium similar to the individual market plan he had in 2013.7

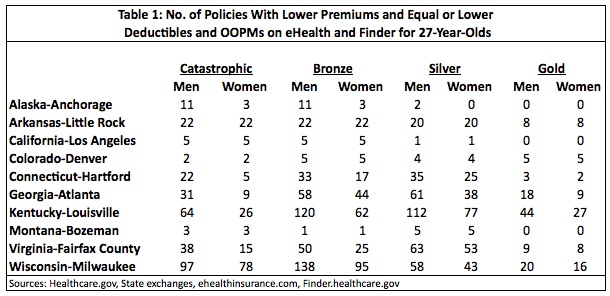

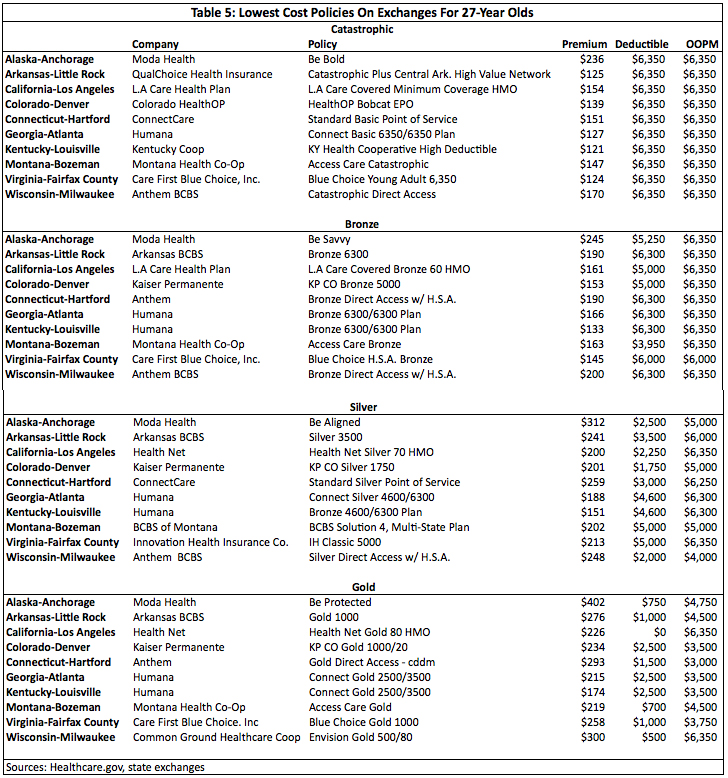

Table 1 shows the number of policies in eHealth and Finder that had lower premiums and lower or equal deductibles and OOPMs compared to the lowest cost exchange policy at the catastrophic, bronze, silver and gold levels for a 27-year-old single person.

Many areas show substantial deterioration on the cost-sharing dimension of quality as a result of ObamaCare. Louisville, Kentucky and Milwaukee, Wisconsin had well over a hundred policies that were of better quality than the lowest-cost policies on the exchanges. However, some places such as Bozeman, Montana and Denver, Colorado displayed only a small deterioration in quality. On balance, though, the exchanges caused quality to decline in these ten areas, with an average of 33 policies between eHealth and Finder that had lower premiums and lower or equal deductibles and OOPMs.

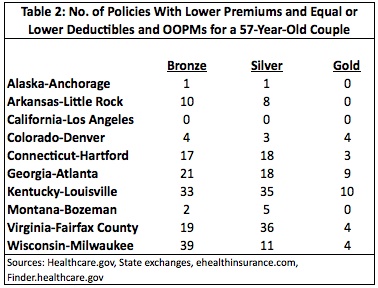

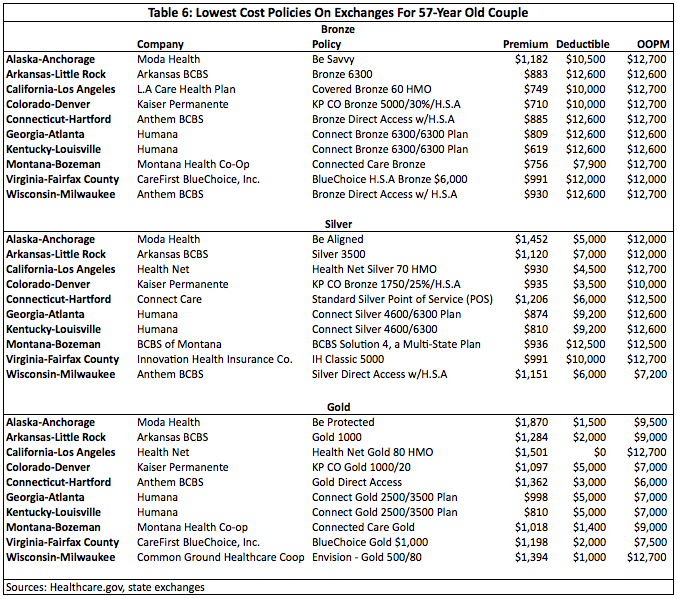

Table 2 shows results for a 57-year-old couple. There are no catastrophic policies here as those are not available to anyone over age 29.

The deterioration in quality is not as sharp as it was for a 27-year-old. There is no decline in quality in Los Angeles, California and very little in Anchorage, Alaska. Nevertheless, there were still dozens of higher-quality policies on eHealth and Finder in areas such as Atlanta, Georgia, Louisville, Kentucky, Fairfax County, Virginia and Milwaukee, Wisconsin. With an average of ten policies between eHealth and Finder that had lower premiums and lower or equal cost-sharing than the lowest-cost policy on the exchanges, the general effect of the exchanges was one of lowering the quality of health insurance for a 57-year-old couple.

Provider Networks

Another dimension of quality is the network of physicians, hospitals and other health care providers available through an insurance plan.

The most restrictive type of network tends to be a health maintenance organization (HMO). HMOs usually require patients to have a primary care physician and to obtain a referral from the primary care physician before seeing a specialist. They generally do not pay for care the patient receives from providers outside the network.

The least restrictive type of network is a preferred provider organization (PPO). Patients do not need to seek a referral from a primary care physician before seeing a specialist under a PPO. PPOs also pay for out-of-network care, although the cost-sharing for seeing an out-of-network provider is generally higher than for in-network providers.

Networks are a more subjective dimension of quality than are out-of-pocket costs. There are many HMOs, such as Kaiser Permanente and Group Health Cooperative, that receive high marks from patients and have reputations for providing very good care. Furthermore, one survey found that, among the people most likely to sign up for coverage on the exchanges, 54 percent preferred plans that cost less even if the network was narrower.8

However, consumer preference is truly revealed by actual dollars spent rather than opinion polls. Data from the employer-based market shows that people tend to prefer less restrictive networks. The Kaiser Family Foundation shows that at the height of HMO coverage in 1996, about 31 percent of employees with employer-provided health insurance were in an HMO plan. By 2013, that had dropped to 14 percent. At the same time, PPOs grew from 28 percent to 57 percent of covered employees.9 Based on actual consumer choice, most of those consumers appear to consider the less restrictive networks of PPOs to be higher quality than HMOs.

There is much anecdotal evidence suggesting networks in the exchange plans are insufficient to meet the preferences of many exchange enrollees. One of the most common complaints about plans on the California exchange is the difficulty of finding a physician.10 Similar complaints have been heard in Connecticut.11 Stories such as these resulted in the pejorative term “skinny network” being given to the networks available through plans on the exchanges.

More substantive research has confirmed the extent of the limited networks available through exchange plans. One survey found that only four of the top 19 cancer centers in the country said they “have access through each of the insurance companies in the state exchange.”12 Dr. Scott Gottlieb examined exchange policies in nine states and found that access to specialists was up to 65 percent lower than in comparable PPO plans.13 Research by McKinsey & Company found narrower hospital networks were more common on the exchanges.14

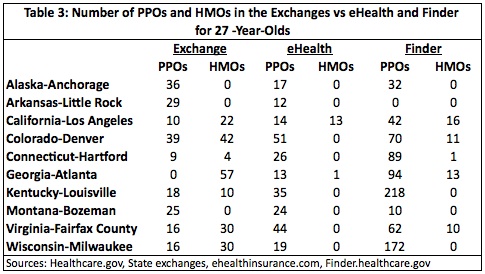

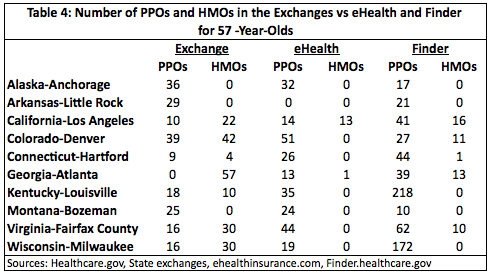

Tables 3 and 4 show how the exchanges compare to eHealth and Finder regarding network quality.

Both tables show somewhat mixed results but with a net deterioration in network quality. Anchorage, Alaska, Little Rock, Arkansas and Bozeman, Montana had slight improvements in quality, with the exchanges having a few more PPO plans than either eHealth or Finder for both single 27-year-olds and 57-year-old-couples.

Network quality declined in seven of the ten areas studied. Two areas, Louisville, Kentucky and Milwaukee, Wisconsin, had 10 and 30 HMO policies, respectively, in their exchanges. Neither had any HMO policies in either eHealth or Finder. Both areas also saw a substantial decline in PPO policies.

Atlanta, Georgia experienced the biggest deterioration in network quality. Finder offered 39 PPO policies and 13 HMO policies while eHealth offered 13 PPOs and one HMO. The exchange offered zero PPO policies and 57 HMO policies.

Overall, the exchanges have resulted in a decline in network quality. In the ten areas studied, Finder had 1,044 more PPO policies than the exchanges while eHealth had 117 more.

Conclusion

Supporters of ObamaCare often claim that health insurance policies on the exchanges are of better quality because they include many benefits that pre-exchange plans did not. ObamaCare mandates that all policies on the exchanges must cover ten “essential health benefits” that include ambulatory patient services, emergency services, hospitalization, maternity and newborn care, mental health and substance use disorder services, prescription drugs, rehabilitative and habilitative services and devices, laboratory services, preventive services and pediatric services. Supporters could argue that some customers are pleased with more benefits even if it means higher out-of-pocket costs and skinnier networks.

Yet the number and type of benefits a plan covers is a far more subjective dimension of quality than out-of-pocket costs or the size of the network. Take, for example, the maternity and newborn benefit. Couples or single women planning to have children would likely find a policy that contained this benefit to be of higher quality than a policy that did not. But many single women, single men and older couples would likely see no value in such a benefit.

Or consider the pediatric services benefit. Adults with children would likely find a policy with that benefit to be a quality policy, while most people without children or those with grown children would be indifferent at best. Yet both of these benefits are required to be included in all exchange plans.

What supporters also overlook is that people who prefer foregoing some benefits for lower out-of-pocket costs and broader networks no longer have that option. In effect, ObamaCare took away the ability to make that trade-off. To keep premiums on the exchanges as low as possible, insurers had little choice but to increase deductibles and OOPMs and make use of “skinny networks” to offset the costs of coverage that ObamaCare mandated.

There is no evidence that ObamaCare improved the overall quality of insurance. There is, however, considerable evidence that it has worsened dimensions of quality such as out-of-pocket costs and size of provider networks. It seems that many people who lost their plans in 2013 and then went to the exchanges noticed a difference. A recent Kaiser Family Foundation survey found that 32 percent of respondents who had to switch to an exchange plan rated the new plan either “not so good” or “poor.”15

Americans deserve many health insurance options that enable them to make the trade-offs that meet their health coverage needs. To achieve that, ObamaCare must be repealed and replaced with a free-market health care system that enables consumers to choose the mix of benefits, out-of-pocket costs and networks that best suit them.

David Hogberg, Ph. D., is senior fellow for health care policy at the National Center for Public Policy Research.

Methodology Notes

-

Policies for 27-year-olds downloaded from eHealthinsurance.com and Finder.healthcare.gov from November 15, 2013 to November 23, 2013. Policies for 57-year-olds downloaded from eHealthinsurance.com and Finder.healthcare.gov from November 30, 2013 to December 15, 2013.

-

Some of the plans on eHealthinsurance.com and Finder.healthcare.gov had separate deductibles for prescription drugs. For those plans, this study added the prescription drug deductibles to both the regular deductible and to the out-of-pocket maximum. For example, if a policy had a $1,000 deductible, a $5,000 out-of-pocket maximum and a prescription drug deductible of $500, this study assumed the deductible was $1,500 and the out-of-pocket maximum was $5,500.

-

In Table 3 and 4, Arkansas has no PPO plans in all but one instance. Many of the plans listed in Arkansas on eHealthinsurance.com and Finder.healthcare.gov were called “Network” plans. Although they looked much like PPO plans, for the purpose of consistency this study did not count them as PPO plans.

-

If a plan appeared in both eHealthinsurance.com and Finder.healthcare.gov, it was counted only once as part of the plans available via eHealthinsurance.com.

Appendix: Lowest Cost Policies On Exchanges

Footnotes:

1 The White House Office of Press Secretary, “Remarks by the President and Governor Deval Patrick on the Affordable Care Act,” October 30, 2013, at http://www.whitehouse.gov/the-press-office/2013/10/30/remarks-president-and-governor-deval-patrick-affordable-care-act (July 14, 2014).

2 Arturo Garcia, “Ed Schultz blames scared media and ‘crappy insurance’ for backlash to Obamacare,” The Raw Story, October 29, 2013.

3 Barnini Chakraborty, “Critics from both sides of the aisle take on Obama’s health care ‘fix’,” FoxNews, November 15, 2013.

4 “Economic Definition of Product Quality,” Economic Glossary, n.d.l., at http://www.glossary.econguru.com/economic-term/product+quality (July 14, 2014).

5 Money Staff, “High deductibles fuel new worries of Obamacare sticker shock,” MSN Money, December 9, 2013.

6 “Deductibles, Out-Of-Pocket Costs, and the Affordable Care Act,” HealthPocket, December 12, 2013, at http://www.healthpocket.com/healthcare-research/infostat/2014-obamacare-deductible-out-of-pocket-costs#.U2QEba1dXd5 (July 11, 2014).

7 Peter Frost, “Obamacare deductibles a dose of sticker shock,” Chicago Tribune, October 13, 2013. Also see Carrie Feibel, “One Texan Weighs Obamacare Options: High Deductible Vs. ‘Huge Fear’,” Kaiser Health News, December 26, 2013; and Carla K. Johnson, “Obamacare enrollees may be hit with high deductibles,” The Leader, December 22, 2013, at http://www.the-leader.com/article/20131222/NEWS/131229947 (September 13, 2014).

8 Bruce Drake, “Kaiser: Potential customers of health exchanges lean towards low-cost, narrower plans,” Fact Tank, Pew Research Center, February 26, 2014, at http://www.pewresearch.org/fact-tank/2014/02/26/likely-customers-of-health-exchanges-lean-towards-low-cost-narrower-plans/ (September 13, 2014).

9 The Kaiser Family Foundation and Health Research & Education Trust, “Employer Health Benefits,” 2013 Annual Survey.

10 Chad Terhune, “Californians gripe about Obamacare enrollment snags, lack of doctors,” Los Angeles Times, May 23, 2014.

11 Arielle Levin Becker, “Latest Obamacare confusion: Exchange plan provider networks,” The CT Mirror, March 12, 2014.

12 Sarah Hurtubise, “Report: Obamacare exchange not covering best hospitals for cancer care,” The Daily Caller, March 19, 2014.

13 Scott Gottlieb, “Challenges of the Affordable Care Act,” Testimony before the Subcommittee on Health of the House Committee on Ways and Means, American Enterprise Institute, December 4, 2013.

14 McKinsey & Company, “Hospital networks: Configurations on the exchanges and their impact premiums,” McKinsey Center for U.S. Health System Reform, December 13, 2013.

15 Liz Hamel, Mira Rao, Larry Levitt, Gary Claxton, Cynthia Cox, Karen Pollitz and Mollyann Brodie, “Survey of Non-Group Health Insurance Enrollees,” Appendix Table 2, Kaiser Family Foundation, June 19, 2013, at http://www.kaiserfamilyfoundation.files.wordpress.com/2014/06/survey-of-non-group-health-insurance-enrollees-appendix-tables-final1.pdf (August 19, 2014).