01 Jun 2015 ObamaCare Premium Hikes for 2016: Ignore Them at Your Own Risk

In early June, the federal government released data on the premium increases that health insurers in 45 states and the District of Columbia are requesting for 2016.1 The numbers were eye-popping, with many requests exceeding 20 percent and a few even exceeding 50 percent. They were definitely “death spiral”-inducing premium hikes. Yet some pundits on the left dismissed them as no big deal.

Over at Mother Jones, Kevin Drum said not to worry, that “we’ve all seen this movie before.”2 Drum claims these are just rates that insurers are requesting. A “few months from now, the real rate increases—the ones approved by state and federal authorities—will begin to trickle out,” he wrote. “They’ll mostly be in single digits, with a few in the low teens. The average for the entire country will end up being something like 4-8 percent.”3

Likewise, Slate’s Jordan Weissman counsels people to relax, that most insurers aren’t requesting big rate hikes. He pointed to the example of Washington State, where the average requested rate increase among 17 insurers was a mere “5.4 percent. Only three of those companies asked for a big enough hike to show up on the federal rate review site. Together, they requested bumps averaging 18 percent, more than three times larger than the actual statewide mean.”4 Some companies guessed wrong about what their costs would be on the exchanges, he contended, and are asking for big premium hikes to compensate. But, said Weissman, there is “a very strong chance we’re talking more about the exceptions rather than the rule.”5

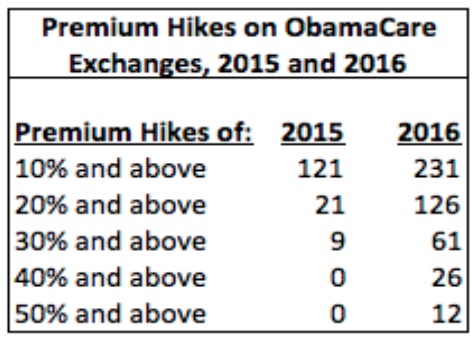

But a closer look at 37 states and D.C. that released data on individual plans on the exchanges (the data the feds released also included small-group plans and plans not sold on the exchange) suggests the situation is more serious than leftist pundits care to admit. For 2015, insurers requested rate increases of at least double digits for 121 policies. For 2016, that has increased to 231. In 2015, rate hikes of over 20 percent were requested for 21 policies and only nine policies had requests of 30 percent or more. In 2016, those numbers are 126 and 61, respectively. Furthermore, there are currently 26 policies with requested rate increases of over 40 percent and 12 of more than 50 percent. There were none for 2015.

This isn’t just a phenomenon that we’ve seen before. It’s a problem that is getting worse.

It is possible, as Drum suggested, that state and federal authorities will force insurers to reduce their rate increases. Yet recent history isn’t really on Drum’s side. Of the 38 exchanges examined, only Kansas, Oregon, Texas and Washington did not approve all of the rate increases insurers requested for 2015. And only one policy was denied the requested rate increase in each of those states.

But for the sake of argument, let’s suppose that state and federal regulators take their machetes to the proposed rate hikes. That won’t be good for the exchanges either. If an insurer needs a 35 percent increase in a policy’s premium to cover costs, and regulators won’t allow the premium to rise more than 20 percent, chances are the insurer will take big losses on that policy again in 2016. If that happens too many times, the insurer will cut its losses and leave the exchange. Fewer insurers means less competition, which will cause premiums to rise even more in the long run.

Weismann may also be correct that these premium hikes are the exception (albeit a growing one), but he fails to acknowledge that they will likely affect consumer behavior. The insurers asking for big rate hikes will likely lose some of their customers, but which ones? Sicker customers face a much bigger burden if they switch to a new insurer, such as having to deal with a new network of physicians and hospitals. Thus, it will likely be healthier customers who flee to cheaper insurers. This means that the insurers asking for big rate hikes for 2016 will end up with even sicker risk pools and have to ask for even higher rate hikes for 2017.

Over time, one of two things will happen to such insurers. Some of their sicker customers will find the constant rate hikes too much and will seek cheaper insurance. Alternatively, the insurers will sustain big losses and eventually exit the market. Their sicker customers will then have little option but to take their business to less costly insurers. Once either of those scenarios happen, those cheaper insurers won’t be cheap for very long.

This is already happening to Time Insurance. Time, a subsidiary of Assurant, is asking for some of the biggest rate hikes among insurers for 2016. Its average premium increase of about 52 percent suggests that its risk pool is heavy on the older and sicker customers. It is likely a big reason Assurant is trying to sell its health insurance business. Even if it can’t, Assurant says it will be out of the health insurance market by the end of 2016.6 Its sicker customers will have to go somewhere, and the unlucky insurers that receive them will eventually have to hike their rates too.

The fact that most exchange policies won’t have rate hikes in the double digits should offer little solace to people who have insurance on the exchanges, and even to ObamaCare supporters. Most likely, and unfortunately, those policies are on borrowed time. Eventually, older and sicker customers will purchase those policies, the rates will go up, and the young and healthy will flee the exchanges. At that point the death spiral will be in full gear. The insurance rate hikes for 2016 are just the beginning.

David Hogberg, Ph. D., is senior fellow for health care policy at the National Center for Public Policy Research.

Endnotes:

1 “Rate Review,” HealthCare.gov, at https://ratereview.healthcare.gov/ (June 10, 2015).

2 Kevin Drum, “Don’t Pay Attention to Obamacare Rate Increase Horror Stories,” Mother Jones, June 2, 2015, at http://www.motherjones.com/kevin-drum/2015/06/dont-pay-attention-obamacare-rate-increase-horror-stories (June 4, 2015).

3 Ibid.

4 Jordan Weissmann, “An Insurer Wants to Raise Its Obamacare Premiums by 85 Percent. Don’t Sweat It,” Slate, June 2, 2015, at http://www.slate.com/blogs/moneybox/2015/06/02/

obamacare_2016_premiums_insurers_ask_for_big_rate_hikes.html (June 4, 2015).

5 Ibid.

6 “Wisconsin-Based Assurant Health Exiting Health Insurance Business,” Insurance Journal, June 11, 2015 at http://www.insurancejournal.com/news/midwest/2015/06/11/371485.htm (June 12, 2015).