01 Oct 2015 Refundable Tax Credits or Large Health Savings Accounts? Let’s Do Both

Executive Summary

There is a big divide on the political right over the tax treatment of health insurance, a divide that threatens to derail any effort to offer a free-market alternative to ObamaCare. One side of the debate favors refundable tax credits for the purchase of health insurance, while the other favors large Health Savings Accounts. Critics of refundable tax credits claim that it is another entitlement, making it similar to the approach of ObamaCare. Critics of large Health Savings Accounts argue that they offer little help to low-income individuals and families, leaving them with few options other than an ineffective Medicaid program.

This National Policy Analysis proposes that the political right offer a free-market health care reform that offers Americans the choice of either a refundable tax credit or a large Health Savings Account. The approach would be tax equitable—that is, everyone would get the same tax benefit regardless of which tax preference he or she chose. Additionally, this NPA proposes using another entitlement, Medicaid, to help fund the refundable tax credits.

Finally, this NPA explains how large Health Savings Accounts can be used to transform the employer-based health insurance system and how this can be done in a politically feasible manner.

The Divide

A big reason that Congress has never voted on a replacement plan to ObamaCare is that there is schism within the Republican Party and the political right more broadly over the proper tax treatment of health insurance. Many prefer the use of refundable tax credits for the purchase of insurance, while others wish to establish large Health Savings Accounts (HSAs). This National Policy Analysis proposes a way to bridge this divide.

Wisconsin Governor Scott Walker and Florida Senator Marco Rubio released plans in August to replace ObamaCare when both were running for the Republican nomination for President (Walker subsequently dropped out). Both plans contained refundable tax credits for the purchase of health insurance.1 A tax credit is a fixed amount that an individual can deduct from his taxes. Thus, if he receives a tax credit of $1,200 to buy insurance, he reduces his tax bill by $1,200. Refundable means that an individual gets the tax credit even if he pays no income taxes. This allows people with little-to-no tax liability—usually people who have lower incomes—to make use of the tax credit as well. Louisiana Governor Bobby Jindal, also a candidate for the Republican nomination, criticized the tax credit proposal. Referring specifically to Walker’s plan, Jindal wrote that it creates “a new entitlement… for every single American human being from the time they are born right up until they grow old and become eligible for Medicare. It is frankly shocking that a Republican candidate for President would author a cradle to grave plan like this.”2 While Jindal acknowledged some of the features in Walker’s plan were good, he dismissed the refundable tax credit as a fundamental acceptance of “the premise of Obamacare—that we need a new federal entitlement program.”3

Jindal is correct. A refundable tax credit is an entitlement, a government program that guarantees access to any citizen who meets the criteria. Under both Walker’s and Rubio’s plans, any person under age 65 who is not in a government health care program like Medicaid or the Veterans Health Administration would be eligible for the tax credit. Entitlements are often tempting fruit to politicians, who find it easy to win reelection by promising to increase spending on them.

Economist John C. Goodman counters that what we face in health care is not a choice between entitlements and no entitlements. Rather, the decision we face is what kind of entitlement we should have:

Here is what Jindal is missing. We already have a health care entitlement. And it’s not likely to ever go away. We are spending billions of dollars on formal programs for low and moderate income families — Medicaid, CHIP, Obamacare, etc. And for everyone who falls through those cracks, we have community health centers, billions of dollars for safety net hospitals and the shifting of costs to paying patients when all of that fails.

Do you want all that money to be spent by non-profit and government institutions, completely free of the disciplines of the marketplace? Or is it better to privatize the funding and allow individual choice and competition to allocate health care dollars?

Democrats have more or less decided how much money we are going to spend on health care and it’s going to be hard for Republicans to roll that back very much. A better use of GOP energy is in deciding how the money is to be spent.4

Other scholars, like the Cato Institute’s Michael Cannon, call for large HSAs instead of tax credits. An HSA is a savings account that can be used to pay for health care expenses and must be coupled with a health insurance policy that has a high deductible. Currently, the policy must have a deductible of $1,300 for a single person and $2,600 for a family to qualify for an HSA. Money put into an HSA is tax free up to the HSA contribution limit. For 2015 the contribution limit is $3,350 for a single person and $6,650 for a family.

Cannon’s proposal for large HSAs increases the contribution limits to $8,000 for an individual and $16,000 for families.5 It also decouples large HSAs from high deductible policies. Rather, an individual or family could pay for their health insurance policy with tax-free funds from the large HSA.

Cannon envisions employers setting up large HSAs for their employees in lieu of providing them with tax-free health insurance. “Large HSAs would let workers take that money as a tax-free HSA contribution, and thereby let taxpayers own and control $9 trillion of their earnings that someone else currently controls,” he states.6 Large HSAs have the added benefit of involving “no income redistribution and create no dependence on government. They would bring health care within reach of those with low-incomes by turning hundreds of millions of other Americans into cost-conscious consumers who force prices downward.”7

Large HSAs would also greatly enhance “portability.” That is, an employee would be able to take his large HSA (and, with it, the health insurance he purchases) from one employer to the next, something that he cannot presently do with employer-provided insurance. Additionally, it would allow Americans to build savings for health care expenses later in life.

Yet, aside from driving down the cost of health care, it is difficult to see how many low-income workers would be helped by large HSAs. First, they are not likely to receive large HSAs from their employers. Only 43 percent of people with a family income that is at 138 percent of the federal poverty or below have an employer who offers insurance, suggesting that such employers of low-income workers do not have the money to fund large HSAs.8 A worker earning, say, $15,000 annually could set up a large HSA on his own, but given his limited means, he would be lucky to be able to contribute a few hundred dollars. And it’s not clear why he would go to the trouble, given that he probably has no income tax liability, and thus would receive no tax break with a large HSA.

Nor do large HSAs give people on Medicaid a chance to escape from it. Medicaid is a command-and-control program that does little to improve the health of its recipients.9 Many recipients would jump at the chance to leave it if they could purchase private insurance. Large HSAs, unfortunately, do not give them that option.

This leaves Cannon’s proposal vulnerable to the charge that it is another benefit for middle and upper class people that offers very little for the poor. That makes large HSAs, on their own, a tough sell politically.

Let’s Do Both

Both sides in this debate favor more choices of health insurance and health care for consumers. Thus, why not give Americans more choices when it comes to the tax treatment of health insurance? Let every American under age 65 have the freedom to choose either a refundable tax credit or a large HSA.

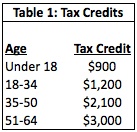

The refundable tax credit would follow the format outlined in Governor Walker’s plan, which has also been proposed in plans by Rep. Tom Price, the 2017 Project and James Capretta. See Table 1:

Americans under age 65 who want to fund their health insurance via a tax credit would simply sign up with the federal government to receive one. The tax credit would be advanceable in that individuals and families would get the tax credit before their bill for insurance came due. They would not have to wait to file their tax returns before receiving the tax credit.

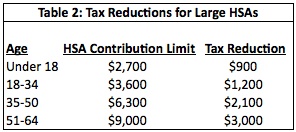

Alternatively, Americans could also fund their health insurance via a large HSA. They would set up a large HSA through a bank or other financial institution and begin contributing money. They would be able to take a tax reduction on their next tax return. The amount a person could contribute to his large HSA would be triple the amount of the refundable tax credit in Table 1, while the tax reduction would be equal to the size of the tax credit. See Table 2:

Thus, an individual age 30 who put $3,600 into a large HSA would be able to reduce his next tax bill by $1,200. If an individual put in less than the contribution limit, his tax reduction would be a percentage based on the amount he put in relative to the contribution limit. So, if that same 30-year-old put in only half ($1,800) of the contribution limit into his large HSA, he would get 50 percent of the tax reduction, or $600.

Thus, an individual age 30 who put $3,600 into a large HSA would be able to reduce his next tax bill by $1,200. If an individual put in less than the contribution limit, his tax reduction would be a percentage based on the amount he put in relative to the contribution limit. So, if that same 30-year-old put in only half ($1,800) of the contribution limit into his large HSA, he would get 50 percent of the tax reduction, or $600.

This system of both refundable tax credits and large HSAs offers many advantages. First, it is a system that is tax-equitable. Everyone gets the same tax reduction, regardless of whether they choose a tax credit or a large HSA.

Next, low-income people who choose a tax credit will not lose their benefit when they earn more income, unlike Medicaid. Medicaid has income limits, and if a poor person exceeds those, he loses his Medicaid benefits. Research suggests Medicaid may discourage poor people from finding ways to increase their income.10 A refundable tax credit creates no such problem as an individual gets the same credit regardless of how much income he makes. Indeed, this reform offers an incentive to earn more income, as a larger income makes setting up a large HSA more feasible.

Third, this system permits people to choose a tax treatment of health insurance that suits their circumstances in life. For example, young people just starting out in life often have relatively low incomes and little income-tax liability. For them, a refundable tax credit might make more sense. A large HSA may make more sense as they grow older and earn more, and thus have the money to put into a large HSA and a tax liability that makes doing so worthwhile.

Finally, the large HSAs in this system will enable people to accumulate health care savings. This will prove useful for two reasons. First, as people grow older and have more health problems, substantial savings in large HSAs will help them pay for increased out-of-pocket costs. Second, Medicare, the government health-care program for people age 65 and older, faces an uncertain future. Its finances may be inadequate to meet the demands that it will face in the next few decades, possibly leading to substantial cuts in the program. Savings put away in large HSAs will help senior citizens endure the shortcomings of a scaled-back Medicare program.

Let One Entitlement Help Fund The Other

Some conservatives and libertarians object that a refundable tax credit is redistributive. They charge that anyone who has less tax liability than the amount of the tax credit is receiving “welfare.” It is usually poor people who have no tax liability, and the U.S. already has a welfare program called Medicaid that pays for health care for the poor.

One way to address this complaint is to reduce Medicaid by the amount of the tax credit for every person who leaves Medicaid and makes use of the tax credit. This way, Medicaid helps fund the tax credit.

Making this work, though, requires Medicaid reform. More specifically, Medicaid must be reformed so that its annual budget is fixed. Currently, Medicaid is an open-ended entitlement program. The federal government must match whatever a state government spends on Medicaid.

Reforming Medicaid so that it is a system of block grants would turn it into a program with a fixed budget. Under that type of system, Medicaid could be reduced by an amount equivalent to the tax credit for every person who leaves the program and claims a tax credit.

Replacing the Employer-Based Tax Exclusion with Large HSAs

This health care reform also offers a way to replace the employer-based tax exclusion for health insurance. Under current law, employees receive a tax break for health insurance, but only if they receive it through their employers. This gives employees an incentive to put every extra dollar of compensation they receive into health insurance, since it is taxed at zero, rather than take it as income, which is taxed at the marginal rate. This system creates many inefficiencies, including incentivizing employees to purchase too much health insurance and encouraging them to overuse health care.

Cannon’s proposal of replacing the employer-based tax exclusion with a system of large HSAs is a good place to start. It would eliminate an inefficient tax break and replace it with a defined benefit. However, it needs a few alterations to make it politically feasible.

First, the tax reduction received by employees who get large HSAs through their employers must be the same as that of people who set up large HSAs on their own. Free-market health care reform could be derailed by charges of unfairness if one group were to receive a larger tax reduction. Thus, employees who receive large HSAs through their employers would receive the same tax reduction that is displayed in Table 2.

Second, the switch from the employer-based tax exclusion to large HSAs must be voluntary. The reason for making it voluntary is that forcing employers and employees to switch is a political non-starter. Making the change mandatory will mean the more than 160 million people who get health coverage through their employers are faced with the prospect of losing their insurance. That would make the ObamaCare events of late 2013 look like a Sunday picnic.

To avoid that, the decision whether or not to switch from the current tax scheme to large HSAs should be left with employers. An employer is in the best position to know when his or her business should make the change and to help his or her employees transition to a system of large HSAs. Employees will be more amenable to having their employers make the change than having it forced on them by politicians.

What are the chances that employers will switch to large HSAs? The history of retirement benefits suggests that, over time, many employers will. From 1980 to 2008, the number of salaried employees participating in “defined benefit” pension plans declined from 38% to 20%. During that same period, the number participating in “defined contribution” 401(k)s increased from 8% to 31%.11 While it is debatable to what extent the employer-based tax exclusion is a defined benefit, there can be little doubt that large HSAs are a defined contribution. With large HSAs, employers will be able to offer employees a benefit that is much more stable — i.e., employers know with some certainty how much health benefits will cost them each year — than the current open-ended tax system which often results in very high premium increases.

HSAs are proving popular with employers and employees, suggesting that a system of large HSAs would also be popular. Approximately 17.4 million Americans were covered by HSA-eligible plans in 2014, an increase over 100 percent since 2009.12 In 2013, HSA plans were offered by 17 percent of employers that offered insurance and 12 percent of workers were enrolled in them.13 HSAs held more than $20 billion in assets, with the average balance being just under $1,300.14 Surveys, including one conducted in 2011 by J.P. Morgan, find very high levels of consumer satisfaction with HSAs as well as sophisticated understanding of how to manage spending.15

Given the advantages of large HSAs over the employer-based tax exclusion, over time more and more employers will switch to large HSAs. The tax exclusion will wither away, and it will do so without the use of government force.

Conclusion

It is possible to bridge the divide on the political right over the tax treatment of health insurance and to do so in a way that offers Americans more choices. Health care reform that includes both refundable tax credits and large HSAs fits the bill.

David Hogberg, Ph. D., is a former senior fellow for health care policy at the National Center for Public Policy Research.

Endnotes:

1 Governor Scott Walker, “The Day One Patient Freedom Plan: My Plan to Repeal & Replace Obamacare,” August 17, 2015, at http://images.politico.com/global/2015/08/17/day_one_patient_freedom_plan.pdf (September 30, 2015); and Senator Marco Rubio, “My Plan To Fix Health Care,” Politico, August 17, 2015, at http://www.politico.com/magazine/story/2015/08/marco-rubio-plan-to-fix-health-care-121453.html (September 30, 2015).

2 Team Jindal, “Jindal: Governor Walker’s Health Care Plan is New Federal Entitlement Program,” Press Release, Bobby Jindal for President, August 18, 2015, at https://www.bobbyjindal.com/jindal-governor-walkers-health-care-plan-is-new-federal-entitlement-program/ (September 30, 2015).

3 Ibid.

4 John C. Goodman, “Why Bobby Jindal Is Wrong About Scott Walker’s Health Plan,” Forbes, August 20, 2015, at http://www.forbes.com/sites/johngoodman/2015/08/20/why-bobby-jindal-is-wrong-about-scott-walkers-health-plan/ (September 30, 2015).

5 Michael F. Cannon, “Large Health Savings Accounts: A Step toward Tax Neutrality for Health Care,” Forum for Health Economics & Policy, 2008, Vol. 11, No. 2, at http://object.cato.org/sites/cato.org/files/articles/cannon-large-health-savings-accounts.pdf (October 10, 2015).

6 Michael F. Cannon, “On health care, Walker and Rubio offer Obamacare lite,” The New Hampshire Union Leader, August 27, 2015, at http://www.unionleader.com/article/20150828/OPINION02/150829238/0/FRONTPAGE (September 30, 2015).

7 Ibid.

8 Hubert Janicki, “Employment-Based Insurance: 2010,” Census Bureau, Household Economic Studies, February 2013, p. 70-134.

9 Katherine Baicker, Sarah L. Taubman, Heidi L. Allen, Mira Bernstein, Jonathan H. Gruber, Joseph P. Newhouse, Eric C. Schneider, Bill J. Wright, Alan M. Zaslavsky, and Amy N. Finkelstein for the Oregon Health Study Group, “The Oregon Experiment—Effects of Medicaid on Clinical Outcomes,” New England Journal of Medicine, May 2, 2013, Vol. 368, No. 18, at http://www.nejm.org/doi/full/10.1056/NEJMsa1212321 (October 10, 2015).

10 Aaron S. Yelowitz, “Evaluating the Effects of Medicaid on Welfare and Work: Evidence from the Past Decade,” Employment Policies Institute, December 2000, at https://www.epionline.org/wp-content/studies/yelowitz_12-2000.pdf (September 30, 2015).

11 Barbara A. Butrica, Howard M. Iams, Karen E. Smith, and Eric J. Toder, “The Disappearing Defined Benefit Pension and Its Potential Impact on the Retirement Incomes of Baby Boomers,” U.S. Social Security Administration, Office of Retirement and Disability Policy, Social Security Bulletin, 2009, Vol. 69, No. 3, at http://www.ssa.gov/policy/docs/ssb/v69n3/v69n3p1.html (October 10, 2015).

12 America’s Health Insurance Plans, “January 2009 Census Shows 8 Million People Covered by HSA/High-Deductible Health Plans,” AHIP Center for Policy And Research, May 2009; and America’s Health Insurance Plans, “January 2014 Census Shows 17.4 Million Enrollees in Health Savings Accounts-Eligible High Deductible Health Plans (HSA/HDHPs),” AHIP Center for Policy And Research, July 2014.

13 The Kaiser Family Foundation, “Employer Health Benefits, 2013 Annual Survey,” August 20, 2013.

14 Kathryn Mayer, “HSA assets top $20 billion,” BenefitsPro, February 12, 2014, at http://www.benefitspro.com/2014/02/12/hsa-assets-top-20-billion (September 30, 2015).

15 J.P. Morgan Chase & Co., “J.P. Morgan releases 2011 Health Savings Accounts customer satisfaction survey results,” Press Release, December 21, 2011, at http://www.4-traders.com/JPMORGAN-CHASE–CO-4831/news/JPMorgan-Chase–Co–JP-Morgan-releases-2011-Health-Savings-Accounts-customer-satisfaction-surve-13943904/ (September 30, 2015).